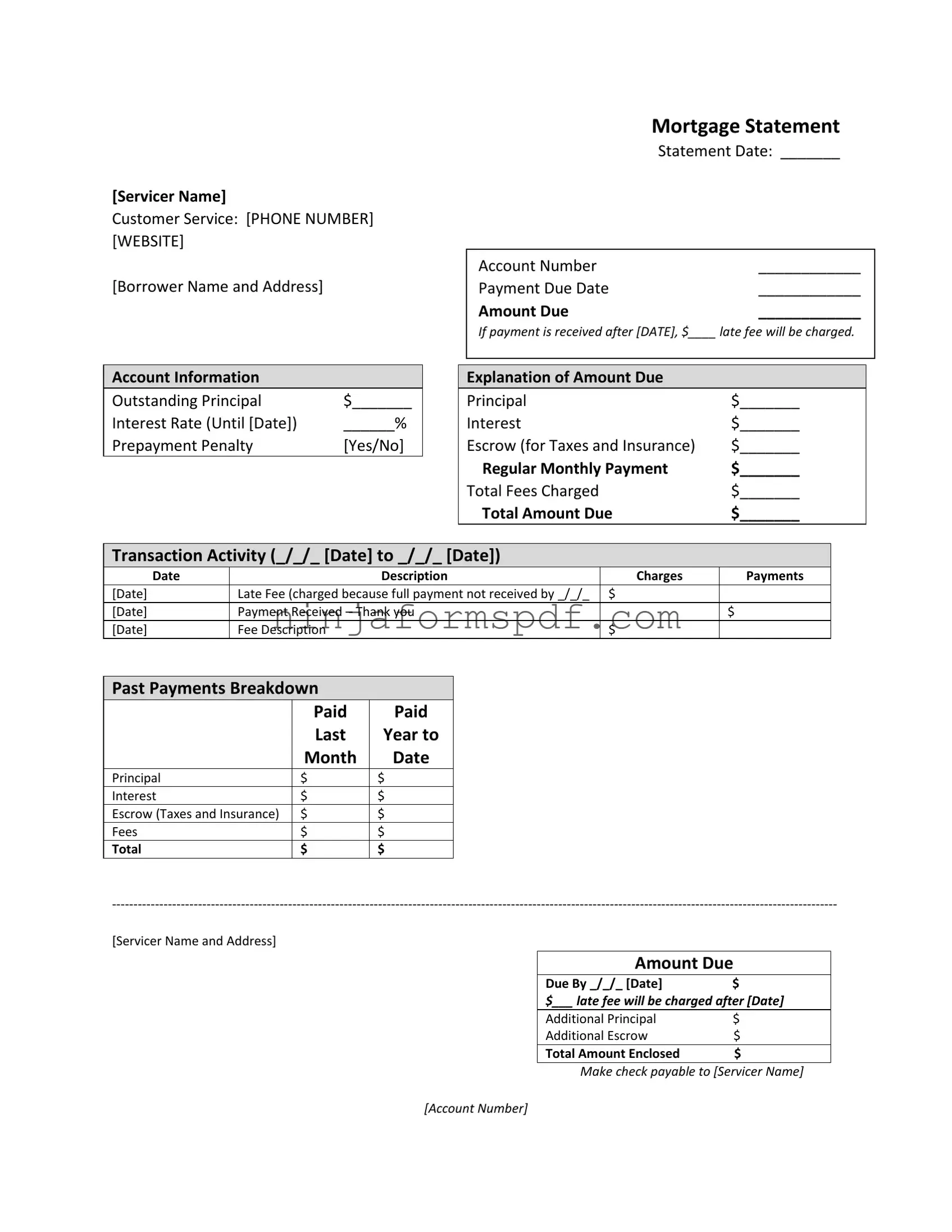

Mortgage Statement Form

Understanding the Mortgage Statement form is crucial for homeowners to manage their mortgage payments effectively. This comprehensive document, issued by the mortgage servicer, outlines essential details such as the borrower's name and address, the statement date, account number, and the payment due date along with the amount. It specifically notifies borrowers of the consequences of late payments, including any late fees that will be applied if the payment is received after the specified date. The statement breaks down the amount due into principal, interest, and escrow (allocated for taxes and insurance), providing a clear overview of where each payment is directed. Moreover, it details the transaction activity within a specific period, showcasing charges, payments received, and any fees charged. An important feature of the statement is the section on past payments, offering a comparative look at payments made in the current and previous year, broken down by principal, interest, escrow, and fees. Furthermore, the document contains critical messages regarding the handling of partial payments and delinquency notices, emphasizing the implications of late or partial payments on the loan's standing. It concludes with instruction for making payments, including the total amount due, payable to the servicer, highlighting the importance of staying informed about the mortgage's current status to avoid adverse outcomes like foreclosure.

Sample - Mortgage Statement Form

[Servicer Name]

Customer Service: [PHONE NUMBER] [WEBSITE]

[Borrower Name and Address]

Mortgage Statement

Statement Date: _______

Account Number |

____________ |

Payment Due Date |

____________ |

Amount Due |

____________ |

If payment is received after [DATE], $____ late fee will be charged.

Account Information

Outstanding Principal |

$_______ |

Interest Rate (Until [Date]) |

______% |

Prepayment Penalty |

[Yes/No] |

Explanation of Amount Due

Principal |

$_______ |

Interest |

$_______ |

Escrow (for Taxes and Insurance) |

$_______ |

Regular Monthly Payment |

$_______ |

Total Fees Charged |

$_______ |

Total Amount Due |

$_______ |

Transaction Activity (_/_/_ [Date] to _/_/_ [Date])

Date |

Description |

Charges |

Payments |

[Date] |

Late Fee (charged because full payment not received by _/_/_ |

$ |

|

[Date] |

Payment Received – Thank you |

|

$ |

[Date] |

Fee Description |

$ |

|

Past Payments Breakdown

|

Paid |

Paid |

|

Last |

Year to |

|

Month |

Date |

Principal |

$ |

$ |

Interest |

$ |

$ |

Escrow (Taxes and Insurance) |

$ |

$ |

Fees |

$ |

$ |

Total |

$ |

$ |

[Servicer Name and Address]

Amount Due

Due By _/_/_ [Date]$

$___ late fee will be charged after [Date]

Additional Principal |

$ |

Additional Escrow |

$ |

Total Amount Enclosed |

$ |

Make check payable to [Servicer Name]

[Account Number]

[Additional tables to be translated]

Important Messages

*Partial Payments: Any partial payments that you make are not applied to your mortgage, but instead are held in a separate suspense account. If you pay the balance of a partial payment, the funds will then be applied to your mortgage.

**Delinquency Notice**

You are late on your mortgage payments. Failure to bring your loan current may result in fees and foreclosure – the loss of your home. As of [Date], you are __ days delinquent on your mortgage loan.

Recent Account History

·Payment due [Date]: Fully paid on time

·Payment due [Date]: Fully paid on [Date]

·Payment due [Date]: Unpaid balance of $________

·Current payment due [Date]: $_______

·Total: $_______ due. You must pay this amount to bring your loan current.

If you are Experiencing Financial Difficulty: See back for information about mortgage counseling or assistance.

Form Information

| Fact Name | Detail |

|---|---|

| Basic Information | The mortgage statement includes basic information such as servicer name, customer service contact details, borrower's name and address, statement date, account number, and the payment due date. |

| Payment Information | Details about the amount due, including if a late fee is applied after a certain date, the regular monthly payment amount, and a breakdown of the amount due including principal, interest, escrow, and any fees. |

| Account Information | Provides a snapshot of the outstanding principal, current interest rate with effective date, and whether there is a prepayment penalty applicable. |

| Transaction Activity | A record of transactions within a specific period, including dates, descriptions, charges, payments, and fees such as late fees. |

| Important Messages | Important notifications about partial payments, delinquency notices, recent account history, and information if experiencing financial difficulty, including mortgage counseling or assistance options. |

Detailed Guide for Writing Mortgage Statement

Filling out a Mortgage Statement form requires attention to detail, as this document is crucial for tracking your mortgage payment history, understanding the breakdown of your monthly payments, and identifying any additional charges or fees you may owe. By carefully entering accurate information in each section of the form, you'll ensure that your mortgage account reflects the correct outstanding balance, interest rate, and any potential late fees or additional payments required. Here's a step-by-step guide to help you navigate through the process:

- Start by entering the name of your Mortgage Servicer in the designated space at the top of the form. This is the company that manages your mortgage and to whom you make your payments.

- Fill in the customer service contact information, including the phone number and website, which is typically provided for your convenience should you have any questions or concerns.

- Write your name and address in the "Borrower Name and Address" section. This identifies you as the mortgage holder and ensures any correspondence or updates reach you directly.

- Enter the statement date, which is the date the statement was issued. This is crucial for maintaining an accurate record of your mortgage account activity.

- Provide your account number. This unique identifier is essential for ensuring that your payments are correctly applied to your mortgage.

- Specify the payment due date. This is the date by which your mortgage payment must be received to avoid any late fees.

- Enter the total amount due for the current payment period. Make sure this includes your principal, interest, and any escrow amounts for taxes and insurance, if applicable.

- If your payment is received after the due date, note the late fee amount that will be charged. This helps you understand the financial consequences of a late payment.

- Under "Account Information," fill in the outstanding principal amount, your current interest rate, and the interest rate's expiry date.

- Indicate whether there is a prepayment penalty by marking "Yes" or "No."

- In the "Explanation of Amount Due" section, break down your payment by listing the amounts allocated to principal, interest, escrow, and any regular monthly payments. Include total fees charged, if any, followed by the total amount due.

- Complete the "Transaction Activity" section by listing any charges, payments, or fee descriptions along with their corresponding dates, to maintain a current and accurate account statement.

- Under "Past Payments Breakdown," provide a summary of the amounts paid towards the principal, interest, escrow, and fees over the last year to the present month date.

- In the space provided at the bottom, fill in the additional principal or escrow amounts you're including with your payment, if any. Then, calculate and enter the total amount enclosed with your payment.

- Lastly, note any important messages or notices from your servicer regarding partial payments, delinquency notices, or instructions if you're experiencing financial difficulty.

Completing the Mortgage Statement form with accurate and up-to-date information is vital for properly managing your mortgage. It not only keeps you informed about your current payment status but also assists in planning and budgeting for future payments. If you encounter any challenges while filling out the form, don't hesitate to contact your Mortgage Servicer's customer service for assistance.

Important Points on Mortgage Statement

What is a Mortgage Statement?

A mortgage statement is a document your mortgage servicer sends you each month. It provides detailed information about your mortgage, including the amount due for that month, your payment due date, and a breakdown of how your payment is applied to the principal, interest, and any escrow account for taxes and insurance. It also outlines any fees charged and displays your loan's outstanding balance and interest rate.

How can I access my Mortgage Statement?

You can access your mortgage statement through your mortgage servicer’s customer service. This can usually be done by logging into your account on their website or contacting them directly via the phone number provided. They will send your mortgage statement each month, either electronically or by mail, based on your preference.

What happens if I make a late payment?

If your payment is received after the specified due date, a late fee will be charged to your account. The exact amount of the late fee and the due date will be detailed in your mortgage statement. It's important to make payments on time to avoid these additional charges.

What is meant by "Interest Rate" on my Mortgage Statement?

The "Interest Rate" listed on your mortgage statement indicates the current percentage of your loan amount that you’re being charged as interest. This rate can be fixed or variable, depending on your loan agreement. The statement may also specify until when this current interest rate is applicable.

What does "Escrow" mean in my Mortgage Statement?

Escrow refers to the funds that your mortgage servicer sets aside each month from your mortgage payment to pay for property taxes and homeowner's insurance on your behalf. The amount allocated for escrow is included in your total monthly payment and detailed in the mortgage statement.

Can I make additional payments to principal or escrow?

Yes, you can make additional payments directly to your principal or escrow. Your mortgage statement typically provides a section where you can specify the amounts you'd like to apply toward additional principal or escrow contributions. These additional payments can help you pay down your loan faster and may reduce the total amount of interest paid over the life of your loan.

What is a suspense account mentioned in the Important Messages?

A suspense account is where your mortgage servicer holds partial payments that are not enough to cover the total monthly payment due. Once you pay the outstanding balance of a partial payment, the funds in the suspense account will then be applied to your mortgage. It's important to complete these partial payments promptly to avoid issues with your loan status.

What should I do if I’m experiencing financial difficulty and can’t make my mortgage payment?

If you're facing financial hardship and are unable to make your mortgage payments, your mortgage statement will often include information about mortgage counseling or assistance programs. These programs can provide guidance and potential solutions to help manage your mortgage payments and avoid foreclosure. It's crucial to contact your mortgage servicer as soon as possible to discuss your options.

Common mistakes

One common mistake people make when filling out the Mortgage Statement form is not verifying the accuracy of their personal information, such as the Borrower Name and Address. This might seem trivial, but discrepancies can lead to significant issues, like misdirected correspondence or even challenges in proving ownership.

Another area often overlooked is the Statement Date and Payment Due Date. It's crucial to note these dates to avoid late payments. A late payment can not only incur additional fees but can also negatively impact one’s credit score.

Mistakes related to the Amount Due section are also common. Borrowers sometimes fail to include the late fee that applies if the payment is received after the specified date. This oversight can lead to an underpayment, further late fees, or other penalties. Paying attention to details mentioned in the mortgage statement regarding due amounts and late fees is therefore essential.

The section detailing Outstanding Principal and Interest Rate is also critical. Errors or misunderstandings here can lead to incorrect payment amounts. Knowing the precise outstanding principal and the interest rate effective until a specific date helps in accurate financial planning and avoids discrepancies in the loan balance.

Ignoring the details about the Escrow account, which covers taxes and insurance, is another mistake. Homeowners must ensure that they understand how much is going into escrow and for what specific purposes those funds are being reserved. Any misunderstanding in this area can lead to shortfalls when taxes and insurance payments are due.

The Transaction Activity and Past Payments Breakdown sections are frequently misunderstood. Reviewing these sections helps borrowers to track their payment history, identify any unrecognized charges, and understand how their payments are being applied towards principal, interest, escrow, and fees.

Lastly, not paying attention to Important Messages such as notices about partial payments, delinquency, and information on assistance if experiencing financial difficulties, is a critical mistake. These sections contain important information regarding the handling of payments and the implications of failing to pay on time, as well as resources for assistance.

Documents used along the form

When managing a mortgage, borrowers and lenders often work with an array of documents beyond the Mortgage Statement form. Each document plays a unique role in the mortgage process, helping to ensure clear communication and legal compliance between the borrower and the lender. Understanding these documents can help borrowers navigate their responsibilities and rights within the realm of property financing.

- Loan Application Form: This form initiates the loan process, collecting the borrower’s personal and financial information for assessment.

- Truth in Lending Disclosure: It outlines the costs of the mortgage, including the APR (Annual Percentage Rate), finance charges, amount financed, and payment schedule, ensuring borrowers are fully informed about their loan costs.

- Good Faith Estimate: This itemized list provides an estimate of all the costs and fees due at closing, giving borrowers a clear view of their potential financial obligation.

- HUD-1 Settlement Statement: A detailed accounting of all transactions, this document is provided at closing showing the actual charges imposed on borrowers and sellers in the real estate sale transaction.

- Deed of Trust/Mortgage: This legal document secures the loan on the property and outlines the terms and conditions under which the loan must be repaid.

- Promissory Note: This document represents the borrower's promise to pay back the loan according to the agreed terms, including interest rates and payment schedules.

- Escrow Disclosure Statement: This shows the use and purpose of the escrow account set up for the payment of property taxes and insurance, detailing the amount to be paid into escrow monthly.

- Loan Estimate: Provided after loan application submission, it offers detailed information about the proposed loan, including interest rate, monthly payments, and total closing costs.

- Closing Disclosure: A final detailed list of all loan terms, this document is provided to the borrower at least three days before closing, highlighting fees, charges, and other crucial loan information.

- Amortization Schedule: This breaks down the repayment of the loan principal and interest over time, showing the borrower exactly how much of each monthly payment goes towards the principal versus interest.

In conclusion, while the Mortgage Statement form is crucial for borrowers to understand their monthly payment obligations, the additional documents listed above are equally important in the mortgage process. They provide transparency, legal security, and the necessary details about the loan terms, fees, and repayment structure. It’s essential for both borrowers and lenders to pay careful attention to these documents to ensure a smooth and legally compliant mortgage process.

Similar forms

The Truth in Lending Act (TILA) Statement, like the Mortgage Statement, provides critical details about the financial terms of a loan. The TILA Statement focuses on informing the borrower about the cost of their loan, including the annual percentage rate (APR), finance charges, and the total amount to be repaid over the life of the loan. While the TILA Statement is broader in scope, both it and the Mortgage Statement serve the crucial role of ensuring borrowers are fully informed about their financial obligations.

A Loan Estimate closely parallels the Mortgage Statement in its purpose of detailing loan information, but it is presented to borrowers earlier in the process, specifically during the loan application phase. This document outlines the estimated interest rate, monthly payment, and total closing costs for a mortgage. Similar to a Mortgage Statement, a Loan Estimate is designed to help borrowers understand the costs associated with their mortgage, albeit at a preliminary stage.

The Closing Disclosure shares similarities with the Mortgage Statement by providing an itemized list of final credits and charges relevant to the mortgage. Given to borrowers just before closing on a home, this document includes the final loan terms, projected monthly payments, and how much the borrower will pay in fees and other costs. Both documents are essential for clarity on the financial responsibilities that accompany a mortgage.

The Annual Escrow Statement, like a Mortgage Statement, offers a detailed account of the escrow portion of a mortgage payment, including property taxes and homeowners insurance. It shows the previous year’s escrow payments and the anticipated requirement for the next year, ensuring homeowners understand how their escrow payments are being allocated and when changes to these payments are necessary.

A Promissory Note, while a more general financial document, shares a fundamental similarity with the Mortgage Statement in that it outlines the borrower's promise to repay a sum to the lender. It specifies the loan amount, interest rate, and repayment terms. Whereas the Mortgage Statement provides a periodic update on the status of such a loan, the Promissory Note is the original agreement that sets these terms.

The Home Equity Line of Credit (HELOC) Statement, similar to the Mortgage Statement, provides an account summary for borrowers who have a line of credit secured against their home's equity. It details the available credit, current balance, interest charges, and minimum payment required. Both statements are crucial for tracking the financial status and obligations of loans secured by real estate.

Monthly Bank Statements, akin to Mortgage Statements, serve the purpose of reporting the activity within an account for a specific period. For a bank account, this includes deposits, withdrawals, fees, and ending balance. The Mortgage Statement is more specialized, focusing on mortgage-related transactions, but the basic principle of account activity tracking is shared between them.

The Credit Card Statement, while distinct in its application to revolving credit rather than installment loans like a mortgage, offers a comparable layout by detailing charges, payments, interest rates, and fees for a specific period. Both statements are vital tools for consumers to manage their debts, understand their financial obligations, and track their payment history.

Dos and Don'ts

When it comes to managing your mortgage, accurate and timely documentation is key. The Mortgage Statement form, a vital piece of paperwork for homeowners, requires careful attention to detail. Here are some dos and don'ts to help ensure that you complete this form correctly and maintain good standing on your mortgage.

Do:- Verify all personal information: Double-check your name, address, and account number for accuracy. Misinformation can lead to processing delays or misapplied payments.

- Confirm payment details: Make sure the payment due date and the amount due are clearly noted and correct. Include late fees if your payment will be submitted after the specified date.

- Understand the breakdown: Review the explanation of the amount due, including principal, interest, and any escrow amounts. This helps you understand exactly where your money is going.

- Check transaction activity: Look at the dates, descriptions, charges, and payments to ensure all recent transactions are listed correctly. This includes monitoring any late fees charged and payments received.

- Ignore incorrect information: If you spot errors, especially in your personal details or account information, contact your servicer immediately. Failing to correct inaccuracies can result in significant issues down the line.

- Skip reading important messages: Vital information, such as notices about partial payments or delinquency warnings, is included for a reason. Not adhering to these messages could compound financial difficulties.

- Forget about the additional options: If you have the ability, consider whether making additional payments towards the principal or escrow could benefit you in the long run. This information should be accurately filled out and included with your payment.

- Dismiss financial difficulty notices: If you're experiencing financial hardship, the form often includes resources for mortgage counseling or assistance. Ignoring these options can lead to missed opportunities for help.

By following these guidelines and paying close attention to the details on your Mortgage Statement form, you can help ensure the smooth management of your mortgage. Should you have any concerns or questions, reaching out to your mortgage servicer directly is always a wise decision.

Misconceptions

Understanding your mortgage statement is crucial for managing your home loan effectively. Yet, many homeowners hold misconceptions about their mortgage statements. Here are four common misunderstandings and the truth behind them:

- Misconception 1: Late Fees Are Negotiable

- Misconception 2: Partial Payments Reduce Principal or Interest

- Misconception 3: The Statement Provides a Complete History of Account Activity

- Misconception 4: If You Pay More Than the Minimum, It Automatically Goes to Principal

Many people believe that late fees shown on the mortgage statement can be negotiated or waived simply by contacting the servicer. However, these fees are typically standardized and based on the terms agreed upon in the mortgage contract. If payment is received after the specified date, a late fee will be charged as clearly stated on the statement.

A common misunderstanding is thinking that any partial payment made goes directly towards reducing the principal or interest. In reality, partial payments are not applied to your mortgage directly. Instead, they are held in a separate suspense account until the balance of the partial payment is paid, at which point it will be applied as specified in the mortgage agreement.

While the mortgage statement does include recent transaction activity, such as charges, payments, and fees, it doesn't cover the entire history of your mortgage account. It shows activity for the current statement period, which could lead to misunderstandings about the overall account status or history.

Many borrowers believe that any amount paid over the minimum required payment will automatically be applied to the principal. However, the actual application of extra funds depends on the servicer's policies. Borrowers usually need to specify that the additional amount should be applied to the principal or it may be put towards future payments or escrow accounts instead.

Understanding the details of your mortgage statement is vital. It helps you track your payments, manage your loan terms effectively, and avoid any misunderstandings. If you have questions or need clarification about your mortgage statement, contacting your servicer directly is the best course of action.

Key takeaways

Understanding the Mortgage Statement is crucial for managing your home loan effectively. Here's what you need to know:

- The statement provides key details such as the Outstanding Principal, Interest Rate, and whether there is a Prepayment Penalty. Keeping an eye on these figures can help you understand how much of your loan is left and how your payments are being applied.

- Due dates and late fees are explicitly stated. This section tells you when your payment is due and the consequences of missing a payment deadline. Late payments can lead to additional charges and, over time, affect your credit score.

- The breakdown of the Amount Due section details your payment allocation, including principal, interest, and escrow. Understanding how your payment is divided can help you see how each payment affects your loan balance over time.

- Transaction Activity and Past Payments Breakdown offer a history of your payments and any charges or fees applied to your account. Regularly reviewing this part can help you track your progress and ensure all payments and charges are accurate.

Moreover, if you find yourself struggling to make payments, the mortgage statement includes important messages regarding partial payments and notices of delinquency. It is also equipped with information on how to seek mortgage counseling or assistance.

Ensuring that your payments are made on time and understanding how those payments are allocated will keep you on track to successfully manage your mortgage. Regular review and comprehension of your mortgage statement are essential steps in achieving this.

Discover Other PDFs

Dnd 5e Character Sheet Fillable - Designed by players for players, this form helps you maintain an up-to-date record of your D&D character's life.

Llc Membership Certificate Template - Ideal for keeping transparent records on the balance of membership interests held after each transaction.