IRS Schedule C 1040 Form

For many individuals running their own businesses, navigating through the complexities of tax documentation is a challenging yet crucial task. Among the essential forms that need tackling is the IRS Schedule C 1040, a tool used to report the income or loss from a business you operated or a profession you practiced as a sole proprietor. This form serves as a vital component for self-employed individuals by allowing them to declare all related income and expenses, ultimately determining the net profit or loss from their business endeavors. Furthermore, the Schedule C influences how much tax is owed to the government or what refund may be expected. Its completion is integral to complying with tax obligations and effectively managing business finances. The careful articulation of expenses and income in Schedule C is not merely about tax filing; it is about understanding the financial health of one's business, optimizing tax outcomes, and planning for future growth. This blend of compliance, strategic financial planning, and direct impact on an individual’s tax liabilities makes the IRS Schedule C 1040 form a critical document for entrepreneurs and freelancers navigating the complexities of tax season.

Sample - IRS Schedule C 1040 Form

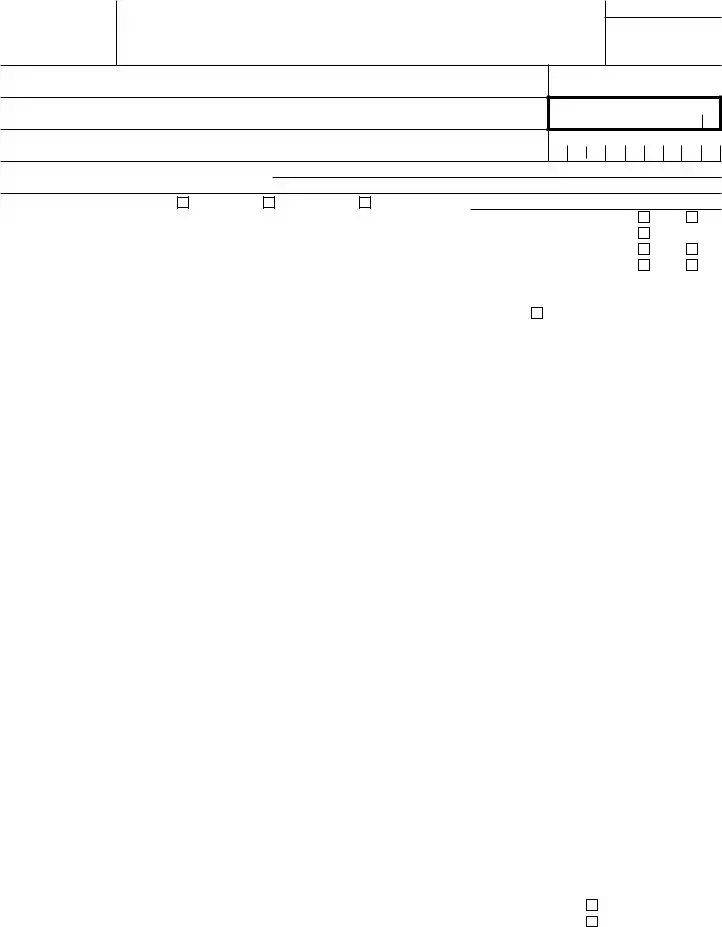

SCHEDULE C (Form 1040)

Department of the Treasury Internal Revenue Service (99)

Profit or Loss From Business

(Sole Proprietorship)

▶Go to www.irs.gov/ScheduleC for instructions and the latest information.

▶Attach to Form 1040,

OMB No.

2021

Attachment Sequence No. 09

Name of proprietor

APrincipal business or profession, including product or service (see instructions)

CBusiness name. If no separate business name, leave blank.

Social security number (SSN)

BEnter code from instructions

▶

DEmployer ID number (EIN) (see instr.)

EBusiness address (including suite or room no.) ▶

City, town or post office, state, and ZIP code

F |

Accounting method: |

(1) |

Cash |

(2) |

|

Accrual |

(3) |

Other (specify) ▶ |

|

|

|

|

|

|

|

||||||

G |

Did you “materially participate” in the operation of this business during 2021? If “No,” see instructions for limit on losses |

. |

Yes |

No |

|||||||||||||||||

H |

If you started or acquired this business during 2021, check here |

. . |

. . |

▶ |

|

|

|||||||||||||||

I |

Did you make any payments in 2021 that would require you to file Form(s) 1099? See instructions . . . |

. . |

. . |

. |

Yes |

No |

|||||||||||||||

J |

If “Yes,” did you or will you file required Form(s) 1099? |

. . |

. . |

. |

Yes |

No |

|||||||||||||||

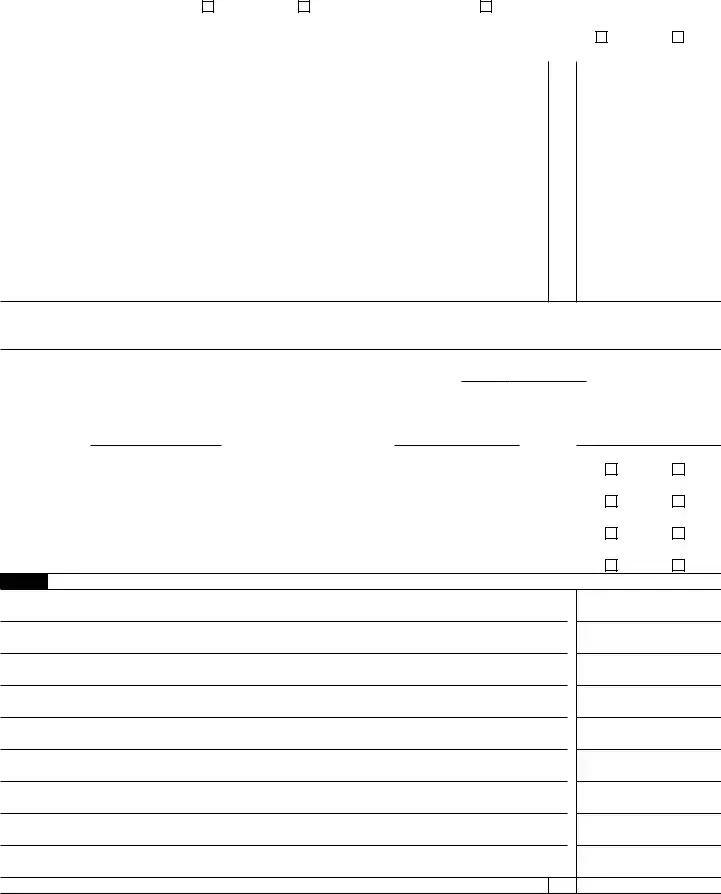

Part I |

Income |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

1 |

Gross receipts or sales. See instructions for line 1 and check the box if this income was reported to you on |

|

|

|

|

|

|||||||||||||||

|

Form |

. . . . . . . . . ▶ |

1 |

|

|

|

|

||||||||||||||

2 |

Returns and allowances |

2 |

|

|

|

|

|||||||||||||||

3 |

Subtract line 2 from line 1 |

3 |

|

|

|

|

|||||||||||||||

4 |

Cost of goods sold (from line 42) |

4 |

|

|

|

|

|||||||||||||||

5 |

Gross profit. Subtract line 4 from line 3 |

5 |

|

|

|

|

|||||||||||||||

6 |

Other income, including federal and state gasoline or fuel tax credit or refund (see instructions) . . . . |

6 |

|

|

|

|

|||||||||||||||

7 |

Gross income. Add lines 5 and 6 |

. . . . . . . . . |

. ▶ |

7 |

|

|

|

|

|||||||||||||

Part II |

Expenses. Enter expenses for business use of your home only on line 30. |

|

|

|

|

|

|

|

|||||||||||||

8 |

Advertising |

8 |

|

|

|

|

|

|

18 |

Office expense (see instructions) . |

18 |

|

|

|

|

||||||

9 |

Car and truck expenses (see |

|

|

|

|

|

|

|

19 |

Pension and |

19 |

|

|

|

|

||||||

|

instructions) . . . . |

9 |

|

|

|

|

|

|

20 |

Rent or lease (see instructions): |

|

|

|

|

|

||||||

10 |

Commissions and fees . |

10 |

|

|

|

|

|

|

a |

Vehicles, machinery, and equipment |

20a |

|

|

|

|

||||||

11 |

Contract labor (see instructions) |

11 |

|

|

|

|

|

|

b |

Other business property . . . |

20b |

|

|

|

|

||||||

12 |

Depletion |

12 |

|

|

|

|

|

|

21 |

Repairs and maintenance . . . |

21 |

|

|

|

|

||||||

13 |

Depreciation and section 179 |

|

|

|

|

|

|

|

22 |

Supplies (not included in Part III) . |

22 |

|

|

|

|

||||||

|

expense deduction |

(not |

|

|

|

|

|

|

|

|

|

|

|

||||||||

|

|

|

|

|

|

|

|

23 |

Taxes and licenses |

23 |

|

|

|

|

|||||||

|

included in Part III) (see |

|

|

|

|

|

|

|

|

|

|

|

|||||||||

|

instructions) . . . . |

13 |

|

|

|

|

|

|

24 |

Travel and meals: |

|

|

|

|

|

|

|

||||

14 |

Employee benefit programs |

|

|

|

|

|

|

|

a |

Travel |

24a |

|

|

|

|

||||||

|

(other than on line 19) |

. |

14 |

|

|

|

|

|

|

b |

Deductible meals (see |

|

|

|

|

|

|

|

|||

15 |

Insurance (other than health) |

15 |

|

|

|

|

|

|

|

instructions) |

24b |

|

|

|

|

||||||

16 |

Interest (see instructions): |

|

|

|

|

|

|

|

25 |

Utilities |

25 |

|

|

|

|

||||||

a |

Mortgage (paid to banks, etc.) |

16a |

|

|

|

|

|

|

26 |

Wages (less employment credits) |

26 |

|

|

|

|

||||||

b |

Other |

16b |

|

|

|

|

|

|

27a |

Other expenses (from line 48) . . |

27a |

|

|

|

|

||||||

17 |

Legal and professional services |

17 |

|

|

|

|

|

|

b |

Reserved for future use . . . |

27b |

|

|

|

|

||||||

28 |

Total expenses before expenses for business use of home. Add lines 8 through 27a |

. ▶ |

28 |

|

|

|

|

||||||||||||||

29 |

Tentative profit or (loss). Subtract line 28 from line 7 |

29 |

|

|

|

|

|||||||||||||||

30 |

Expenses for business use of your home. Do not report these expenses elsewhere. Attach Form 8829 |

|

|

|

|

|

|||||||||||||||

|

unless using the simplified method. See instructions. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||

|

Simplified method filers only: Enter the total square footage of (a) your home: |

|

|

|

|

|

|

|

|||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||

|

and (b) the part of your home used for business: |

|

|

|

|

|

|

|

. Use the Simplified |

|

|

|

|

|

|||||||

|

Method Worksheet in the instructions to figure the amount to enter on line 30 |

30 |

|

|

|

|

|||||||||||||||

31 |

Net profit or (loss). Subtract line 30 from line 29. |

|

|

|

|

|

|

|

} |

|

|

|

|

|

|

||||||

|

• If a profit, enter on both Schedule 1 (Form 1040), line 3, and on Schedule SE, line 2. (If you |

|

|

|

|

|

|

||||||||||||||

|

checked the box on line 1, see instructions). Estates and trusts, enter on Form 1041, line 3. |

|

31 |

|

|

|

|

||||||||||||||

|

• If a loss, you must go to line 32. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||

32 |

If you have a loss, check the box that describes your investment in this activity. See instructions. |

} |

|

|

|

|

|

|

|||||||||||||

|

• If you checked 32a, enter the loss on both Schedule 1 (Form 1040), line 3, and on Schedule |

|

|

|

|

|

|

||||||||||||||

|

SE, line 2. (If you checked the box on line 1, see the line 31 instructions.) Estates and trusts, enter on |

|

32a |

All investment is at risk. |

|||||||||||||||||

|

Form 1041, line 3. |

|

|

|

|

|

|

|

|

|

|

|

|

|

32b |

Some investment is not |

|||||

|

• If you checked 32b, you must attach Form 6198. Your loss may be limited. |

|

|

|

at risk. |

|

|

||||||||||||||

For Paperwork Reduction Act Notice, see the separate instructions. |

|

|

Cat. No. 11334P |

|

|

|

Schedule C (Form 1040) 2021 |

||||||||||||||

Schedule C (Form 1040) 2021 |

Page 2 |

|

Part III |

Cost of Goods Sold (see instructions) |

|

33 |

Method(s) used to |

|

|

|

|

|

|

|

value closing inventory: |

a |

Cost |

b |

Lower of cost or market |

c |

Other (attach explanation) |

34Was there any change in determining quantities, costs, or valuations between opening and closing inventory?

If “Yes,” attach explanation |

Yes |

No

35 |

Inventory at beginning of year. If different from last year’s closing inventory, attach explanation . . . |

35 |

36 |

Purchases less cost of items withdrawn for personal use |

36 |

37 |

Cost of labor. Do not include any amounts paid to yourself |

37 |

38 |

Materials and supplies |

38 |

39 |

Other costs |

39 |

40 |

Add lines 35 through 39 |

40 |

41 |

Inventory at end of year |

41 |

42 |

Cost of goods sold. Subtract line 41 from line 40. Enter the result here and on line 4 |

42 |

Part IV Information on Your Vehicle. Complete this part only if you are claiming car or truck expenses on line 9 and are not required to file Form 4562 for this business. See the instructions for line 13 to find out if you must file Form 4562.

43 |

When did you place your vehicle in service for business purposes? (month/day/year) |

▶ |

/ |

/ |

44Of the total number of miles you drove your vehicle during 2021, enter the number of miles you used your vehicle for:

a |

Business |

b Commuting (see instructions) |

c Other |

45 |

Was your vehicle available for personal use during |

||

46 |

Do you (or your spouse) have another vehicle available for personal use? |

||

47a |

Do you have evidence to support your deduction? |

||

b |

If “Yes,” is the evidence written? |

||

Yes

Yes

Yes

Yes

No

No

No

No

Part V Other Expenses. List below business expenses not included on lines

48 |

Total other expenses. Enter here and on line 27a |

48

Schedule C (Form 1040) 2021

Form Information

| Fact Name | Description |

|---|---|

| Purpose of Schedule C (Form 1040) | Used by sole proprietors and single-member LLCs to report business profits or losses. |

| Eligibility for Use | Individuals operating a business as the sole proprietor or as a disregarded entity are required to file. |

| Reporting Requirements | Income, expenses, and the net profit or loss of a business must be reported and may affect personal income tax liability. |

| Impact on Tax Calculations | The net profit or loss as reported on Schedule C is used to calculate self-employment tax owed, under the Self-Employment Contributions Act. |

| Attachment and Filing | Schedule C is filed with the personal income tax return, IRS Form 1040, and is subject to the same filing deadline. |

Detailed Guide for Writing IRS Schedule C 1040

Filling out the IRS Schedule C 1040 form is a critical process for individuals who operate a sole proprietorship or single-member LLC. This form is used to report income or loss from a business you operated or a profession you practiced as the sole proprietor. Accurately completing this form is essential for compliance with tax laws and to ensure the correct calculation of taxable income. The following steps will guide you through each part of the form, helping you to provide the necessary information accurately and efficiently.

- Start by gathering all necessary documentation including receipts, bank statements, and records of expenses and income related to your business.

- In Part I, Income, report the gross receipts or sales from your business. Subtract returns and allowances to find the gross income, then calculate and enter the cost of goods sold if applicable. The result will be your gross profit.

- In Part II, Expenses, list all business expenses in the categories provided. Be accurate and include only allowable expenses such as advertising, car and truck expenses, rents, wages, and other business expenses.

- If applicable, fill out Part III, Cost of Goods Sold, which details the method and calculations used to determine the cost of inventory sold during the year.

- In Part IV, Information on Your Vehicle, complete this section only if you are claiming vehicle expenses. Provide information about the vehicle's use in the business, including mileage, personal and business use percentage, and if applicable, evidence of expenses.

- Part V, Other Expenses, is for listing any other business expenses not reported in Part II. Provide a description and the amount for each expense.

- Review the form to ensure all information is complete and accurate. Double-check your math and ensure that all income and expenses are accurately reported.

- Sign and date the form. By signing, you are declaring that the information is accurate to the best of your knowledge.

- Attach Schedule C to your Form 1040 or 1040-SR and submit it to the IRS, either electronically or by mail, by the tax filing deadline.

Completing the IRS Schedule C 1040 form with thoroughness and accuracy is vital for reporting your business earnings and calculating your tax liability correctly. Take the time to review the instructions for each section and consult a tax professional if you have questions or concerns. Remember, submitting accurate and timely information is your responsibility and plays a critical role in managing your business's financial health.

Important Points on IRS Schedule C 1040

What is the IRS Schedule C 1040 form?

The IRS Schedule C 1040 form is a tax document used by sole proprietors and single-member LLCs to report their business income and expenses. The information on this form helps determine the net profit or loss of the business, which is then reported on the individual's personal tax return. This form is essential for anyone who operates a business on their own.

Who needs to file a Schedule C 1040 form?

Anyone who operates a sole proprietorship or a single-member LLC and has earned income from business activities should file a Schedule C form alongside their standard 1040 tax return. This includes freelancers, independent contractors, and small business owners who have not incorporated their businesses.

What kind of information do I need to complete Schedule C?

To accurately complete Schedule C, you will need detailed records of all your business income and expenses. This includes gross receipts from sales or services, cost of goods sold, advertising expenses, home office expenses, vehicle expenses, and any other costs incurred while operating your business. Keeping meticulous records throughout the year will make filling out Schedule C easier and more accurate.

Can I deduct expenses on Schedule C?

Yes, a variety of business expenses can be deducted on Schedule C. These deductions can include the cost of goods sold, home office expenses, business use of your car, and marketing costs, among others. By deducting these expenses, you can lower your taxable income, thus reducing the amount of tax you owe. However, it's important to ensure that all deductions are legitimate business expenses and are well-documented in case of an IRS audit.

What happens if I show a loss on Schedule C?

Showing a loss on Schedule C is not necessarily a bad thing; it may happen, especially in the early years of a business. If you report a loss, this will reduce your overall taxable income, possibly lowering your tax liability. In some cases, if your losses are substantial and extend over several years, the IRS may scrutinize whether your business is a genuine profit-seeking endeavor or a hobby. Therefore, maintaining detailed records and evidence of your efforts to make the business profitable is crucial.

How does a Schedule C impact my self-employment tax?

The net profit reported on Schedule C not only affects your income tax but also your self-employment tax, which covers Social Security and Medicare taxes for individuals who work for themselves. Essentially, if your business is profitable, you will need to pay self-employment tax on that income. This is an important consideration for budgeting and financial planning for anyone self-employed.

Where can I find help with filling out my Schedule C?

If you're unsure about how to complete your Schedule C or if you have complex business transactions, seeking the help of a tax professional can be beneficial. Certified Public Accountants (CPAs) and enrolled agents can provide guidance and ensure that your return is accurate. Additionally, there are various tax preparation software options available that can simplify the process, especially if your business transactions are straightforward.

Common mistakes

One common mistake people make when filling out the IRS Schedule C 1040 form is not accurately reporting all their income. This includes not only the revenue from sales of goods or services but also any miscellaneous income. Inaccuracies in income reporting can lead to audits and penalties, impacting the taxpayer's financial integrity.

Another prevalent error is the incorrect classification of expenses. Business expenses must be both ordinary and necessary. However, individuals often misinterpret these criteria, either inadvertently classifying personal expenses as business ones or vice versa. This misclassification can lead to an inaccurate representation of business profit and may attract scrutiny from the IRS.

Mixing business with personal expenses on the Schedule C form is a significant pitfall. Separate accounts for business and personal transactions are advisable to ensure clarity. When expenses are combined, it becomes challenging to substantiate business expenses during an IRS audit, potentially leading to the disallowance of valid business expense claims.

Not fully understanding the home office deduction is another common mistake. The IRS has specific requirements defining what constitutes a dedicated workspace in one's home. Misunderstanding these requirements can lead to incorrect claims, which might increase the risk of an audit. It's crucial to accurately measure the space used exclusively for business and calculate the deduction based on IRS guidelines.

Inaccurately calculating car and truck expenses can also be problematic. Whether choosing to deduct actual expenses or use the standard mileage rate, keeping detailed records is essential. Many overlook the necessity to document the purpose, distance, and expenses associated with each trip, potentially leading to issues with the deduction's validity.

A lack of adequate documentation for deductions claimed on Schedule C can lead to reversals during an audit. Receipts, invoices, and logs should be maintained to substantiate expenses. Failure to keep these records can make it difficult to defend expenses if questioned by the IRS.

An oversight in identifying and deducting all potentially deductible taxes is another error. Not all taxes paid in the course of business are obvious, and some may be inadvertently overlooked, such as certain state and local sales taxes, excise taxes, and real estate taxes on business property.

Forgetting to carry over a net operating loss (NOL) to subsequent years is a missed opportunity. Businesses experiencing more expenses than income can apply this loss to reduce taxable income in future years, but it often goes unclaimed due to misunderstanding or oversight.

Lastly, a common mistake is not seeking professional advice when needed. The complexities of the IRS Schedule C form can be daunting, and inaccuracies can have significant implications. Professional guidance can help ensure accuracy, compliance, and optimization of tax benefits.

Documents used along the form

The IRS Schedule C 1040 form is an essential document for many self-employed individuals and sole proprietors, detailing profits and losses from a business. However, to accurately complete this form and comply with tax regulations, several other documents and forms are often required. These materials support the information entered on the Schedule C and ensure the proper calculation of taxable income and allowable deductions.

- 1099-NEC, Nonemployee Compensation: This form is used to report income received as an independent contractor or freelancer. Since these earnings are subject to self-employment tax, they must be declared on Schedule C.

- 1040-ES, Estimated Tax for Individuals: Individuals who expect to owe $1,000 or more when their return is filed need to make estimated tax payments throughout the year. This form helps calculate and pay these taxes quarterly, crucial for avoiding penalties.

- 8829, Expenses for Business Use of Your Home: For those who use a part of their home for business, this form calculates the deductible expenses related to business use. This can include portions of rent, utilities, and repairs.

- 4562, Depreciation and Amortization: This form is necessary for reporting the depreciation of property or amortization of assets over time. It supports the deductions listed on Schedule C for equipment and other assets used in the business.

- Profit and Loss Statement: While not a formal IRS document, a profit and loss statement is critical for summarizing the revenues, costs, and expenses during a period. This statement is often used to fill out the Schedule C accurately.

- Receipts and Records of Expenses: Keeping detailed records and receipts for all business-related expenses is vital. These documents substantiate the deductions claimed on the Schedule C and can be crucial in case of an audit.

In preparing the Schedule C, these documents play a pivotal role in ensuring that all income is reported and all allowable expenses are deducted, which culminates in an accurate representation of a business's financial status to the IRS. Careful attention to compiling and reviewing these forms can significantly ease the tax preparation process and contribute to the successful management of one's business finances.

Similar forms

The IRS Schedule C 1040 form is closely related to the IRS Schedule 1 Form 1040, as both are integral to the U.S. individual income tax return system. Schedule 1 is used to report additional income or adjustments to income that are not directly entered on the main Form 1040. This includes earnings from rental, real estate, partnerships, S corporations, trusts, and more, as well as deductions like student loan interest and educator expenses. It complements the Schedule C by providing a broader scope of non-employment income and deductions information.

Similarly, the IRS Schedule SE (Self-Employment Tax) form parallels the Schedule C 1040 in its audience—individuals who have earned income from self-employment. This form is used to calculate the tax due on net earnings from self-employment, which is necessary because self-employed individuals do not have Social Security and Medicare taxes automatically withheld from their income. The income reported on Schedule C helps determine the figure entered on Schedule SE.

The IRS Form 1040-ES, Estimated Tax for Individuals, also shares similarities with Schedule C, particularly for self-employed individuals or those who earn income outside of regular employment. This form is used to estimate and pay quarterly taxes on income that isn't subject to withholding taxes, including earnings reported on Schedule C. It ensures taxpayers remain in compliance by making regular payments on expected tax liabilities throughout the year.

The Schedule C is akin to the IRS Form 8829, Expenses for Business Use of Your Home, in that both are used by individuals who operate businesses. Form 8829 is specifically for those who dedicate part of their home for business purposes, allowing them to calculate and deduct expenses related to this use. These expenses can affect the profit or loss reported on Schedule C.

IRS Form 1099-MISC, Miscellaneous Income, and IRS Form 1099-NEC, Nonemployee Compensation, are both tightly connected to the information reported on Schedule C. These forms are typically received by freelancers, independent contractors, and others who are self-employed, detailing the income they've earned from various clients over the fiscal year. This income must then be reported on Schedule C when filing taxes.

The IRS Form 4562, Depreciation and Amortization, relates to Schedule C due to its focus on business assets. This form allows taxpayers to calculate and report depreciation and amortization of business property, which can significantly impact the net income or loss reported on Schedule C by lowering taxable income through deductions related to the cost of business assets.

IRS Schedule E (Form 1040), Supplemental Income and Loss, is similar to Schedule C but serves individuals who earn income from rental real estate, royalties, partnerships, S corporations, trusts, and estates rather than from operating a business or being self-employed. The form details how to report this type of income and the expenses associated with it, which can have implications for the taxpayer's overall income situation.

The IRS Form 8853, Archer MSAs and Long-Term Care Insurance Contracts, while not directly related to business operations, indirectly connects with Schedule C for individuals who have medical savings accounts (MSAs) related to their self-employed business. Contributions and distributions to these accounts, including those for long-term care insurance, can affect an individual’s financial landscape, including how they report income or deductions related to their business.

IRS Form 1040, the U.S. Individual Income Tax Return, is essentially the foundation to which Schedule C is attached. The main form consolidates the taxpayer's income, deductions, and credits to calculate their total tax liability or refund. Schedule C feeds into this overarching form by detailing the profit or loss from a business, influencing the taxpayer’s adjusted gross income and ultimately their tax liability.

Lastly, the IRS Form W-9, Request for Taxpayer Identification Number and Certification, although not a tax return form, relates to the process of reporting and filing taxes for business owners who utilize the Schedule C. Freelancers and independent contractors often complete this form for their clients, enabling the accurate reporting of their income through forms like the 1099-NEC, which is then reported on Schedule C. This chain of documentation is crucial for accurate income reporting and tax calculation.

Dos and Don'ts

Filing the IRS Schedule C 1040 form is a critical process for individuals who operate a business as a sole proprietor or an independent contractor. To ensure accuracy and compliance, here are crucial dos and don'ts to consider:

Do:Ensure all information is complete and accurate. Double-check your figures and the spelling of names and addresses.

Report all income from your business, including cash, checks, and credit card transactions, to avoid underreporting.

Deduct legitimate business expenses that are ordinary and necessary, such as supplies, rent, and utilities.

Utilize the correct IRS documentation for guidance, especially when calculating deductions and expenses.

Maintain clear and detailed records of all transactions, receipts, and expenses throughout the year to support your filings.

Mix personal expenses with business expenses. Keeping them separate simplifies reporting and can prevent issues down the line.

Forget to include home office expenses if you use a portion of your home exclusively for business on a regular basis.

Omit small amounts of income. All income, regardless of the amount, must be reported to the IRS.

Underestimate the importance of filing on time. Late filing can result in penalties and interest on any taxes owed.

Adhering to these guidelines will help ensure that your Schedule C 1040 form is accurately completed, reducing the likelihood of errors and the potential for an audit. It is advisable to consult with a tax professional if you have questions or concerns about your specific situation.

Misconceptions

Many people have misconceptions about the IRS Schedule C (Form 1040) used for reporting income and expenses from a business you operated or a profession you practiced as a sole proprietor. Below are six common misunderstandings and clarifications to help provide a clearer understanding.

- Schedule C is only for "big" businesses. One of the most common misconceptions is that Schedule C is intended solely for large, established businesses. In reality, it's used by anyone who operates a business or practices a profession on their own, regardless of the size of their operation. This includes people who sell goods online, freelance, or run a small service.

- If you didn't make a profit, you don't have to file Schedule C. Even if your business didn't turn a profit, you are still required to file Schedule C if you have business income. Reporting your expenses could result in a net loss, which might lower your overall taxable income, potentially reducing your tax liability.

- You can deduct personal expenses as business expenses. Only expenses that are both ordinary (common in your trade or business) and necessary (helpful and appropriate for your business) are deductible. Personal expenses are not deductible as business expenses, even if they seem related to the business.

- Filing Schedule C increases the chance of an IRS audit. There's a misconception that filing a Schedule C automatically raises red flags with the IRS, increasing the likelihood of an audit. While it's true that sole proprietors may face audits, accurate and complete record-keeping can significantly reduce this risk. It's more about the accuracy of what's reported than the simple act of filing.

- Income reported on Schedule C is exempt from Social Security and Medicare taxes. Another common misunderstanding is that income reported on Schedule C is only subject to federal income tax. However, net earnings from self-employment are also subject to Social Security and Medicare taxes, collectively known as self-employment tax and reported on Schedule SE.

- You do not need to keep detailed records if you file Schedule C. Some people believe that a lack of detailed records is acceptable if they file Schedule C, assuming a simple summary of income and expenses will suffice. However, the IRS requires detailed records of all income and expenses reported on Schedule C to verify the accuracy of your tax return and support your deductions.

Understanding these misconceptions about Schedule C can help individuals better prepare for and accurately file their taxes, potentially saving them time and minimizing issues with the IRS.

Key takeaways

The IRS Schedule C 1040 form is essential for individuals who operate a sole proprietorship or single-member LLC. This form is used to report the income or loss from a business they operate or a profession they practice as the sole proprietor. Understanding the key aspects of this form can help in accurate and beneficial filing. Here are four critical takeaways when filling out and using the IRS Schedule C 1040 form.

- Accurately Report Income and Expenses: To ensure an accurate representation of the business's financial health, it's critical to meticulously report all income the business received and all expenses it incurred during the tax year. This includes income from sales, services, and any other business-related income, along with expenses like rent, supplies, and other costs necessary to operate the business.

- Understand the Impact on Self-Employment Taxes: The net profit or loss calculated on Schedule C not only affects the income tax owed but also determines the self-employment taxes. These are contributions to Social Security and Medicare. A proper understanding of how to calculate these taxes is important, as they represent a significant part of the tax responsibilities for self-employed individuals.

- Consider Deductions Carefully: Several deductions are available to sole proprietors that can significantly reduce taxable income. These include deductions for home office expenses, vehicle use, depreciation, and expenses related to business travel, meals, and entertainment. Each deduction has specific requirements and limits, so it's essential to understand these rules to maximize potential benefits.

- Keep Accurate and Detailed Records: Good record-keeping is crucial for filling out Schedule C accurately and efficiently. This involves keeping receipts, invoices, bank statements, and logs of business-related expenses and income throughout the year. In the event of an audit, having detailed records will support the amounts reported on Schedule C.

By grasping these fundamental aspects, individuals can confidently manage and report their business finances, potentially reduce their tax liability, and avoid issues with the IRS.

Discover Other PDFs

CBP Declaration Form 6059B - Travelers use this form to declare items purchased or acquired abroad, including gifts and souvenirs.

I864 Form - Understanding the obligations as a sponsor before signing the I-864 form is crucial.