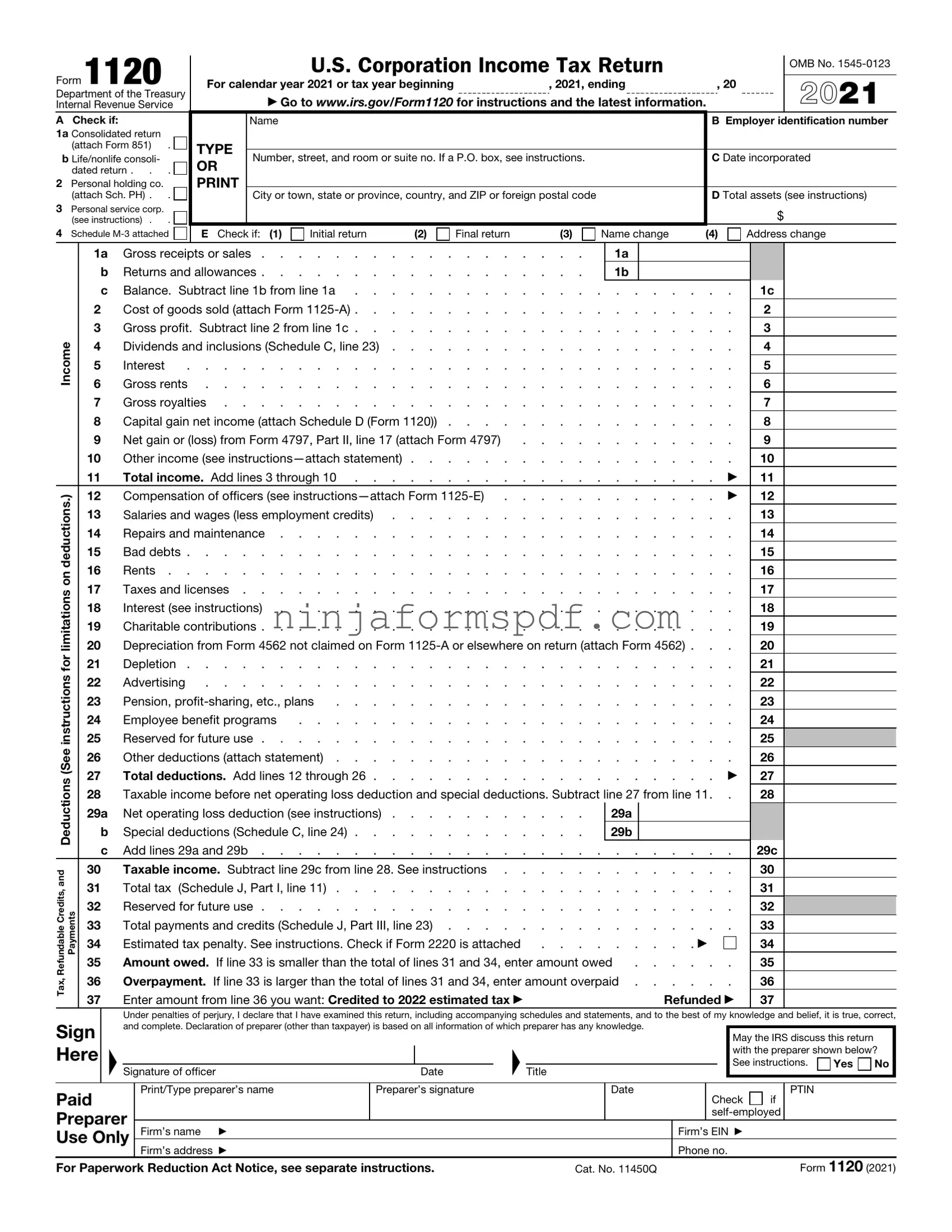

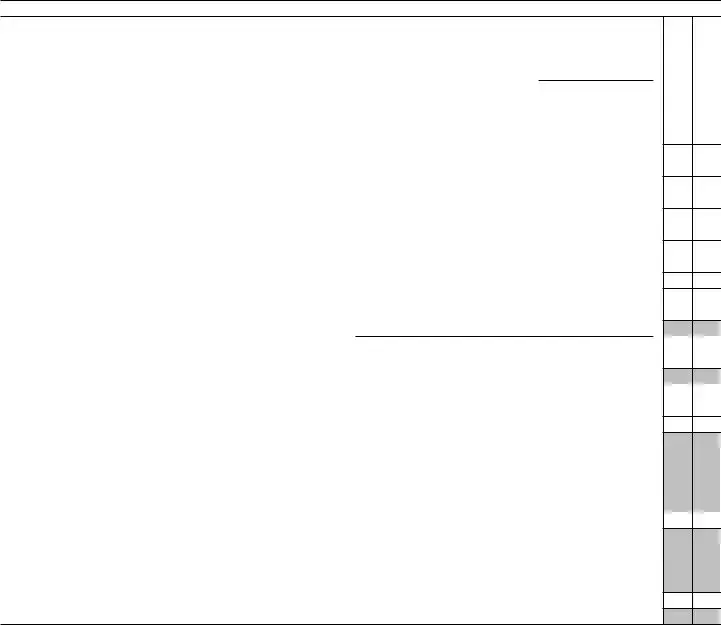

IRS 1120 Form

Filing taxes is a task that every business in the U.S. undertakes annually, and for corporations, the IRS 1120 form is a critical component of this process. This form serves as the primary reporting vehicle through which corporations communicate their income, gains, losses, deductions, and credits to the Internal Revenue Service (IRS). Its complexity can often seem daunting due to the detailed financial information required, including but not limited to, reporting earnings and profits, dividend distributions, and taxable income adjustments. Moreover, the form plays a crucial role in determining the corporation's tax liability for the year, making it essential for businesses to approach this document with accuracy and thoroughness. The IRS 1120 form not only ensures compliance with federal tax laws but also impacts a corporation's financial planning and strategy for the upcoming year. Understanding its components, deadlines, and the potential for penalties or audits associated with misfiling is key to a corporation's financial health and legal standing.

Sample - IRS 1120 Form

Form 1120

Department of the Treasury

Internal Revenue Service

A Check if:

1a Consolidated return (attach Form 851) .

b Life/nonlife consoli- dated return . . .

2Personal holding co. (attach Sch. PH) . .

3Personal service corp. (see instructions) . .

4 Schedule

|

|

U.S. Corporation Income Tax Return |

|

|

OMB No. |

||||

|

|

|

|

||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

For calendar year 2021 or tax year beginning |

|

, 2021, ending |

, 20 |

|

2021 |

||||

|

▶ Go to www.irs.gov/Form1120 for instructions and the latest information. |

|

|||||||

|

Name |

|

|

|

|

|

B Employer identification number |

||

TYPE |

|

|

|

|

|

|

|

|

|

Number, street, and room or suite no. If a P.O. box, see instructions. |

|

C Date incorporated |

|||||||

OR |

|

||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

City or town, state or province, country, and ZIP or foreign postal code |

|

D Total assets (see instructions) |

|||||||

|

|

||||||||

|

|

|

|

|

|

|

|

$ |

|

E Check if: (1) |

Initial return |

(2) |

Final return |

(3) |

Name change |

(4) |

Address change |

||

|

1a |

|

Gross receipts or sales |

|

. . . |

. |

|

1a |

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||

|

|

b |

|

Returns and allowances |

|

. . . |

. |

|

1b |

|

|

|

|

|

|

|

|

|

|

|

|

||||||||

|

|

c |

|

Balance. Subtract line 1b from line 1a |

|

. . . . . . . . . . . . |

1c |

|

|

||||||||||||||||||||

|

2 |

|

|

Cost of goods sold (attach Form |

|

. . . . . . . . . . . . |

2 |

|

|

|

|||||||||||||||||||

|

3 |

|

|

Gross profit. Subtract line 2 from line 1c |

|

. . . . . . . . . . . . |

3 |

|

|

|

|||||||||||||||||||

Income |

4 |

|

|

Dividends and inclusions (Schedule C, line 23) |

|

. . . . . . . . . . . . |

4 |

|

|

|

|||||||||||||||||||

5 |

|

|

Interest |

. . . . . . . . . . . . . . . . . . |

|

. . . . . . . . . . . . |

5 |

|

|

|

|||||||||||||||||||

|

|

|

|

|

|

|

|||||||||||||||||||||||

|

6 |

|

|

Gross rents |

|

. . . . . . . . . . . . |

6 |

|

|

|

|||||||||||||||||||

|

7 |

|

|

Gross royalties |

|

. . . . . . . . . . . . |

7 |

|

|

|

|||||||||||||||||||

|

8 |

|

|

Capital gain net income (attach Schedule D (Form 1120)) . . . . |

|

. . . . . . . . . . . . |

8 |

|

|

|

|||||||||||||||||||

|

9 |

|

|

Net gain or (loss) from Form 4797, Part II, line 17 (attach Form 4797) |

|

. . . . . . . . . . . . |

9 |

|

|

|

|||||||||||||||||||

|

10 |

|

|

Other income (see |

|

. . . . . . . . . . . . |

10 |

|

|

|

|||||||||||||||||||

|

11 |

|

|

Total income. Add lines 3 through 10 |

|

. . . |

. |

. . |

. . |

. |

. |

. |

|

▶ |

11 |

|

|

|

|||||||||||

deductions.) |

12 |

|

|

Compensation of officers (see |

|

. . . |

. |

. . |

. . |

. |

. |

. |

|

▶ |

12 |

|

|

|

|||||||||||

13 |

|

|

Salaries and wages (less employment credits) |

|

. . . . . . . . . . . . |

13 |

|

|

|

||||||||||||||||||||

|

|

|

|

|

|

|

|||||||||||||||||||||||

|

14 |

|

|

Repairs and maintenance |

|

. . . . . . . . . . . . |

14 |

|

|

|

|||||||||||||||||||

|

15 |

|

|

Bad debts |

|

. . . . . . . . . . . . |

15 |

|

|

|

|||||||||||||||||||

on |

16 |

|

|

Rents |

|

. . . . . . . . . . . . |

16 |

|

|

|

|||||||||||||||||||

17 |

|

|

Taxes and licenses |

|

. . . . . . . . . . . . |

17 |

|

|

|

||||||||||||||||||||

limitations |

|

|

|

|

|

|

|||||||||||||||||||||||

20 |

|

|

Depreciation from Form 4562 not claimed on Form |

20 |

|

|

|

||||||||||||||||||||||

|

18 |

|

|

Interest (see instructions) |

|

. . . . . . . . . . . . |

18 |

|

|

|

|||||||||||||||||||

|

19 |

|

|

Charitable contributions |

|

. . . . . . . . . . . . |

19 |

|

|

|

|||||||||||||||||||

for |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||

21 |

|

|

Depletion |

|

. . . . . . . . . . . . |

21 |

|

|

|

||||||||||||||||||||

instructions |

25 |

|

|

Reserved for future use |

|

. . . . . . . . . . . . |

25 |

|

|

|

|||||||||||||||||||

|

22 |

|

|

Advertising |

|

. . . . . . . . . . . . |

22 |

|

|

|

|||||||||||||||||||

|

23 |

|

|

Pension, |

. . . . . . . . . . |

|

. . . . . . . . . . . . |

23 |

|

|

|

||||||||||||||||||

|

24 |

|

|

Employee benefit programs |

. . . . . . . . . . . . |

|

. . . . . . . . . . . . |

24 |

|

|

|

||||||||||||||||||

(See |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

26 |

|

|

Other deductions (attach statement) |

|

. . . . . . . . . . . . |

26 |

|

|

|

||||||||||||||||||||

|

|

|

|

|

|

|

|||||||||||||||||||||||

Deductions |

27 |

|

|

Total deductions. Add lines 12 through 26 |

|

. . . |

. |

. . |

. . |

. |

. |

. |

|

▶ |

27 |

|

|

|

|||||||||||

28 |

|

|

Taxable income before net operating loss deduction and special deductions. Subtract line 27 from line 11. . |

28 |

|

|

|

||||||||||||||||||||||

|

|

|

|

|

|

||||||||||||||||||||||||

|

29a |

|

Net operating loss deduction (see instructions) |

|

. . . |

. |

|

29a |

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||

|

|

b |

|

Special deductions (Schedule C, line 24) |

|

. . . |

. |

|

29b |

|

|

|

|

|

|

|

|

|

|

|

|

||||||||

|

|

c |

|

Add lines 29a and 29b |

|

. . . . . . . . . . . . |

29c |

|

|

||||||||||||||||||||

and |

30 |

|

|

Taxable income. Subtract line 29c from line 28. See instructions . |

|

. . . . . . . . . . . . |

30 |

|

|

|

|||||||||||||||||||

31 |

|

|

Total tax |

(Schedule J, Part I, line 11) |

|

. . . . . . . . . . . . |

31 |

|

|

|

|||||||||||||||||||

Credits,Refundable Payments |

|

|

|

|

|

|

|||||||||||||||||||||||

32 |

|

|

Reserved for future use |

|

. . . . . . . . . . . . |

32 |

|

|

|

||||||||||||||||||||

|

33 |

|

|

Total payments and credits (Schedule J, Part III, line 23) . . . . |

|

. . . . . . . . . . . . |

33 |

|

|

|

|||||||||||||||||||

|

34 |

|

|

Estimated tax penalty. See instructions. Check if Form 2220 is attached |

. . |

. |

. . |

. . |

. |

. ▶ |

|

|

|

34 |

|

|

|

||||||||||||

|

35 |

|

|

Amount owed. If line 33 is smaller than the total of lines 31 and 34, enter amount owed |

. . . . . . |

35 |

|

|

|

||||||||||||||||||||

Tax, |

36 |

|

|

Overpayment. If line 33 is larger than the total of lines 31 and 34, enter amount overpaid |

36 |

|

|

|

|||||||||||||||||||||

37 |

|

|

Enter amount from line 36 you want: Credited to 2022 estimated tax ▶ |

|

|

|

|

|

|

|

Refunded ▶ |

37 |

|

|

|

||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||

Sign |

|

|

Under penalties of perjury, I declare that I have examined this return, including accompanying schedules and statements, and to the best of my knowledge and belief, it is true, correct, |

||||||||||||||||||||||||||

|

|

and complete. Declaration of preparer (other than taxpayer) is based on all information of which preparer has any knowledge. |

|

|

|

|

|

May the IRS discuss this return |

|

||||||||||||||||||||

Here |

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

with the preparer shown below? |

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

See instructions. |

Yes |

No |

||

|

|

|

▲Signature of officer |

|

|

|

Date |

▲ |

|

Title |

|

|

|

|

|

|

|

|

|

|

|||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Paid |

|

|

Print/Type preparer’s name |

|

|

Preparer’s signature |

|

|

|

|

|

Date |

|

|

|

|

|

Check |

if |

PTIN |

|

|

|||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||

Preparer |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||

Firm’s name ▶ |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Firm’s EIN ▶ |

|

|

|

|

|||||||||

Use Only |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||

Firm’s address ▶ |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Phone no. |

|

|

|

|

|

||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||

For Paperwork Reduction Act Notice, see separate instructions. |

|

|

|

Cat. No. 11450Q |

|

|

|

|

|

|

|

Form 1120 (2021) |

|||||||||||||||||

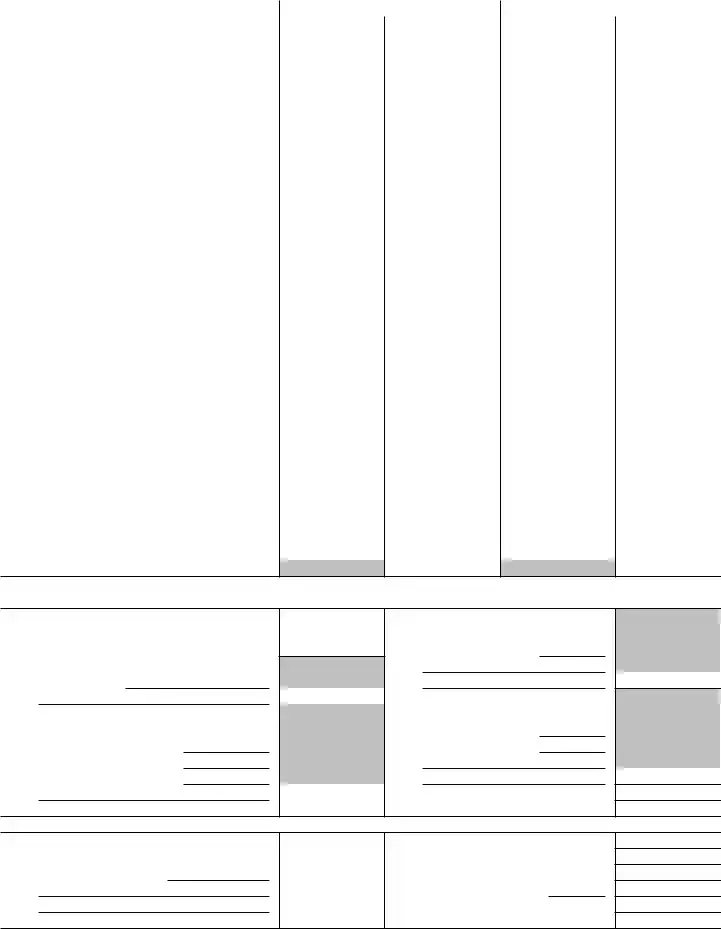

Form 1120 (2021) |

|

|

Page 2 |

|

Schedule C |

Dividends, Inclusions, and Special Deductions (see |

(a) Dividends and |

(b) % |

(c) Special deductions |

|

instructions) |

inclusions |

(a) × (b) |

|

|

|

|||

1Dividends from

stock) |

50 |

2Dividends from

|

stock) |

65 |

|

|

See |

3 |

Dividends on certain |

instructions |

4 |

Dividends on certain preferred stock of |

23.3 |

5 |

Dividends on certain preferred stock of |

26.7 |

6 |

Dividends from |

50 |

7 |

Dividends from |

65 |

8 |

Dividends from wholly owned foreign subsidiaries |

100 |

|

|

See |

9 |

Subtotal. Add lines 1 through 8. See instructions for limitations |

instructions |

10Dividends from domestic corporations received by a small business investment

|

company operating under the Small Business Investment Act of 1958 |

100 |

11 |

Dividends from affiliated group members |

100 |

12 |

Dividends from certain FSCs |

100 |

13

|

corporation (excluding hybrid dividends) (see instructions) |

|

100 |

|

|

14 |

Dividends from foreign corporations not included on line 3, 6, 7, 8, 11, 12, or 13 |

|

|

||

|

(including any hybrid dividends) |

|

|

|

|

15 |

Reserved for future use |

|

|

|

|

16a |

Subpart F inclusions derived from the sale by a controlled foreign corporation (CFC) of |

|

|

||

|

the stock of a |

100 |

|

||

|

(see instructions) |

|

|

||

b |

Subpart F inclusions derived from hybrid dividends of tiered corporations (attach Form(s) |

|

|

||

|

5471) (see instructions) |

|

|

|

|

c |

Other inclusions from CFCs under subpart F not included on line 16a, 16b, or 17 (attach |

|

|

||

|

Form(s) 5471) (see instructions) |

|

|

||

17 |

Global Intangible |

18 |

|

19 |

|

20 |

Other dividends |

21 |

Deduction for dividends paid on certain preferred stock of public utilities . . . . |

22 |

Section 250 deduction (attach Form 8993) |

23Total dividends and inclusions. Add column (a), lines 9 through 20. Enter here and on page 1, line 4 . . . . . . . . . . . . . . . . . . . . . .

24 |

Total special deductions. Add column (c), lines 9 through 22. Enter here and on page 1, line 29b |

Form 1120 (2021)

Form 1120 (2021) |

|

|

|

|

|

Page 3 |

|

Schedule J |

Tax Computation and Payment (see instructions) |

|

|

|

|

|

|

Part |

|

|

|

|

|

||

1 |

Check if the corporation is a member of a controlled group (attach Schedule O (Form 1120)). See instructions |

▶ |

|

|

|||

2 |

Income tax. See instructions |

. . . . |

. . . |

2 |

|

||

3 |

Base erosion minimum tax amount (attach Form 8991) |

. . . . |

. . . |

3 |

|

||

4 |

Add lines 2 and 3 |

. . . . |

. . . |

4 |

|

||

5a |

Foreign tax credit (attach Form 1118) |

5a |

|

|

|

|

|

b |

Credit from Form 8834 (see instructions) |

5b |

|

|

|

|

|

c |

General business credit (attach Form 3800) |

5c |

|

|

|

|

|

d |

Credit for prior year minimum tax (attach Form 8827) |

5d |

|

|

|

|

|

e |

Bond credits from Form 8912 |

5e |

|

|

|

|

|

6 |

Total credits. Add lines 5a through 5e |

. . . . |

. . . |

6 |

|

||

7 |

Subtract line 6 from line 4 |

. . . . |

. . . |

7 |

|

||

8 |

Personal holding company tax (attach Schedule PH (Form 1120)) |

. . . . |

. . . |

8 |

|

||

9a |

Recapture of investment credit (attach Form 4255) |

9a |

|

|

|

|

|

b |

Recapture of |

9b |

|

|

|

|

|

c |

Interest due under the |

|

|

|

|

|

|

|

Form 8697) |

9c |

|

|

|

|

|

d |

Interest due under the |

9d |

|

|

|

|

|

e |

Alternative tax on qualifying shipping activities (attach Form 8902) |

9e |

|

|

|

|

|

f |

Interest/tax due under section 453A(c) and/or section 453(l) |

9f |

|

|

|

|

|

g |

Other (see |

9g |

|

|

|

|

|

10 |

Total. Add lines 9a through 9g |

. . . . |

. . . |

10 |

|

||

11 |

Total tax. Add lines 7, 8, and 10. Enter here and on page 1, line 31 |

. . . . |

. . . |

11 |

|

||

Part

12 Reserved for future use . . . . . . . . . . . . . . . . . . . . . . . . . . .

12

Part

13 |

2020 overpayment credited to 2021 |

. . . . . . . . |

13 |

|

|

||

14 |

2021 estimated tax payments |

. . . . . . . . |

14 |

|

|

||

15 |

2021 refund applied for on Form 4466 |

. . . . . . . . |

15 |

( |

) |

||

16 |

Combine lines 13, 14, and 15 |

. . . . . . . . |

16 |

|

|

||

17 |

Tax deposited with Form 7004 |

. . . . . . . . |

17 |

|

|

||

18 |

Withholding (see instructions) |

. . . . . . . . |

18 |

|

|

||

19 |

Total payments. Add lines 16, 17, and 18 |

. . . . . . . . |

19 |

|

|

||

20 |

Refundable credits from: |

|

|

|

|

|

|

a |

Form 2439 |

|

20a |

|

|

|

|

b |

Form 4136 |

|

20b |

|

|

|

|

c |

Reserved for future use |

|

20c |

|

|

|

|

d |

Other (attach |

|

20d |

|

|

|

|

21 |

Total credits. Add lines 20a through 20d |

. . . . . . . . |

21 |

|

|

||

22 |

Reserved for future use |

. . . . . . . . |

22 |

|

|

||

23 |

Total payments and credits. Add lines 19 and 21. Enter here and on page 1, line 33 . |

. . . . . . . . |

23 |

|

|

||

|

|

|

|

|

|

|

Form 1120 (2021) |

Form 1120 (2021) |

Page 4 |

Schedule K Other Information (see instructions)

1 |

Check accounting method: a |

Cash |

b |

Accrual |

c |

Other (specify) ▶ |

2See the instructions and enter the: a Business activity code no. ▶

b Business activity ▶ c Product or service ▶

3 Is the corporation a subsidiary in an affiliated group or a

If “Yes,” enter name and EIN of the parent corporation ▶

4At the end of the tax year:

aDid any foreign or domestic corporation, partnership (including any entity treated as a partnership), trust, or

corporation’s stock entitled to vote? If “Yes,” complete Part I of Schedule G (Form 1120) (attach Schedule G) . . . . . .

bDid any individual or estate own directly 20% or more, or own, directly or indirectly, 50% or more of the total voting power of all

classes of the corporation’s stock entitled to vote? If “Yes,” complete Part II of Schedule G (Form 1120) (attach Schedule G) .

5At the end of the tax year, did the corporation:

aOwn directly 20% or more, or own, directly or indirectly, 50% or more of the total voting power of all classes of stock entitled to vote of any foreign or domestic corporation not included on Form 851, Affiliations Schedule? For rules of constructive ownership, see instructions. If “Yes,” complete (i) through (iv) below.

Yes No

(i)Name of Corporation

(ii)Employer

Identification Number

(if any)

(iii)Country of Incorporation

(iv)Percentage Owned in Voting

Stock

bOwn directly an interest of 20% or more, or own, directly or indirectly, an interest of 50% or more in any foreign or domestic partnership (including an entity treated as a partnership) or in the beneficial interest of a trust? For rules of constructive ownership, see instructions. If “Yes,” complete (i) through (iv) below.

(i)Name of Entity

(ii)Employer

Identification Number

(if any)

(iii)Country of Organization

(iv)Maximum

Percentage Owned in Profit, Loss, or Capital

6During this tax year, did the corporation pay dividends (other than stock dividends and distributions in exchange for stock) in

excess of the corporation’s current and accumulated earnings and profits? See sections 301 and 316 . . . . . . . .

If “Yes,” file Form 5452, Corporate Report of Nondividend Distributions. See the instructions for Form 5452. If this is a consolidated return, answer here for the parent corporation and on Form 851 for each subsidiary.

7At any time during the tax year, did one foreign person own, directly or indirectly, at least 25% of the total voting power of all classes of the corporation’s stock entitled to vote or at least 25% of the total value of all classes of the corporation’s stock? .

For rules of attribution, see section 318. If “Yes,” enter:

(a) Percentage owned ▶ |

and (b) Owner’s country ▶ |

(c)The corporation may have to file Form 5472, Information Return of a 25%

8 Check this box if the corporation issued publicly offered debt instruments with original issue discount . . . . . . ▶

If checked, the corporation may have to file Form 8281, Information Return for Publicly Offered Original Issue Discount Instruments.

If checked, the corporation may have to file Form 8281, Information Return for Publicly Offered Original Issue Discount Instruments.

9Enter the amount of

10Enter the number of shareholders at the end of the tax year (if 100 or fewer) ▶

11If the corporation has an NOL for the tax year and is electing to forego the carryback period, check here (see instructions) ▶

If the corporation is filing a consolidated return, the statement required by Regulations section

12Enter the available NOL carryover from prior tax years (do not reduce it by any deduction reported on

page 1, line 29a.) . . . . . . . . . . . . . . . . . . . . . . . . . ▶ $

Form 1120 (2021)

Form 1120 (2021) |

Page 5 |

Schedule K Other Information (continued from page 4)

13 |

Are the corporation’s total receipts (page 1, line 1a, plus lines 4 through 10) for the tax year and its total assets at the end of the |

Yes No |

|

||

|

tax year less than $250,000? |

|

|

If “Yes,” the corporation is not required to complete Schedules L, |

|

|

distributions and the book value of property distributions (other than cash) made during the tax year ▶ $ |

|

14 |

Is the corporation required to file Schedule UTP (Form 1120), Uncertain Tax Position Statement? See instructions . . . . |

|

|

If “Yes,” complete and attach Schedule UTP. |

|

15a |

Did the corporation make any payments in 2021 that would require it to file Form(s) 1099? |

|

b |

If “Yes,” did or will the corporation file required Form(s) 1099? |

|

16During this tax year, did the corporation have an

own stock? . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

17During or subsequent to this tax year, but before the filing of this return, did the corporation dispose of more than 65% (by value)

of its assets in a taxable,

18Did the corporation receive assets in a section 351 transfer in which any of the transferred assets had a fair market basis or fair

market value of more than $1 million? . . . . . . . . . . . . . . . . . . . . . . . . . . .

19During the corporation’s tax year, did the corporation make any payments that would require it to file Forms 1042 and

20 Is the corporation operating on a cooperative basis?. . . . . . . . . . . . . . . . . . . . . . .

21During the tax year, did the corporation pay or accrue any interest or royalty for which the deduction is not allowed under section

267A? See instructions . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

If “Yes,” enter the total amount of the disallowed deductions ▶ $

22Does the corporation have gross receipts of at least $500 million in any of the 3 preceding tax years? (See sections 59A(e)(2)

and (3)) . |

. |

. |

. |

. |

. |

. |

. |

. |

. |

. |

. |

. |

. |

. |

. |

. |

. |

. |

. |

. |

. |

. |

. |

. |

. |

. |

. |

. |

. |

. |

. |

. |

. |

. |

. |

If “Yes,” complete and attach Form 8991.

23Did the corporation have an election under section 163(j) for any real property trade or business or any farming business in effect

|

during the tax year? See instructions |

24 |

Does the corporation satisfy one or more of the following? See instructions |

aThe corporation owns a

bThe corporation’s aggregate average annual gross receipts (determined under section 448(c)) for the 3 tax years preceding the current tax year are more than $26 million and the corporation has business interest expense.

cThe corporation is a tax shelter and the corporation has business interest expense. If “Yes,” complete and attach Form 8990.

25 |

Is the corporation attaching Form 8996 to certify as a Qualified Opportunity Fund? |

|

If “Yes,” enter amount from Form 8996, line 15 . . . . ▶ $ |

26Since December 22, 2017, did a foreign corporation directly or indirectly acquire substantially all of the properties held directly or indirectly by the corporation, and was the ownership percentage (by vote or value) for purposes of section 7874 greater than 50% (for example, the shareholders held more than 50% of the stock of the foreign corporation)? If “Yes,” list the ownership

percentage by vote and by value. See instructions . . . . . . . . . . . . . . . . . . . . . . .

Percentage: By Vote |

By Value |

Form 1120 (2021)

Form 1120 (2021) |

|

|

|

|

|

|

|

|

|

|

|

|

Page 6 |

||

Schedule L |

|

Balance Sheets per Books |

|

|

Beginning of tax year |

|

|

End of tax year |

|

||||||

|

|

|

Assets |

|

|

|

|

(a) |

|

(b) |

|

(c) |

|

|

(d) |

1 |

Cash |

|

|

|

|

|

|

|

|

|

|

||||

2a |

Trade notes and accounts receivable . . . |

|

|

|

|

|

|

|

|

|

|||||

b |

Less allowance for bad debts . . |

. . . |

|

( |

|

) |

|

( |

) |

|

|

||||

3 |

Inventories |

|

|

|

|

|

|

|

|

|

|||||

4 |

U.S. government obligations |

. . . . . |

|

|

|

|

|

|

|

|

|

|

|||

5 |

|

|

|

|

|

|

|

|

|

|

|||||

6 |

Other current assets (attach statement) . . |

|

|

|

|

|

|

|

|

|

|

||||

7 |

Loans to shareholders |

|

|

|

|

|

|

|

|

|

|

||||

8 |

Mortgage and real estate loans |

|

|

|

|

|

|

|

|

|

|

||||

9 |

Other investments (attach statement) . . . |

|

|

|

|

|

|

|

|

|

|

||||

10a |

Buildings and other depreciable assets . . |

|

|

|

|

|

|

|

|

|

|||||

b |

Less accumulated depreciation . . |

. . . |

|

( |

|

) |

|

( |

) |

|

|

||||

11a |

Depletable assets |

|

|

|

|

|

|

|

|

|

|||||

b |

Less accumulated depletion . . . |

. . . |

|

( |

|

) |

|

( |

) |

|

|

||||

12 |

Land (net of any amortization) |

|

|

|

|

|

|

|

|

|

|||||

13a |

Intangible assets (amortizable only) |

. . . |

|

|

|

|

|

|

|

|

|

|

|||

b |

Less accumulated amortization . . |

. . . |

|

( |

|

) |

|

( |

) |

|

|

||||

14 |

Other assets (attach statement) |

|

|

|

|

|

|

|

|

|

|

||||

15 |

Total assets |

|

|

|

|

|

|

|

|

|

|||||

|

Liabilities and Shareholders’ Equity |

|

|

|

|

|

|

|

|

|

|||||

16 |

Accounts payable |

|

|

|

|

|

|

|

|

|

|

||||

17 |

Mortgages, notes, bonds payable in less than 1 year |

|

|

|

|

|

|

|

|

|

|

||||

18 |

Other current liabilities (attach statement) . . |

|

|

|

|

|

|

|

|

|

|

||||

19 |

Loans from shareholders |

|

|

|

|

|

|

|

|

|

|

||||

20 |

Mortgages, notes, bonds payable in 1 year or more |

|

|

|

|

|

|

|

|

|

|

||||

21 |

Other liabilities (attach statement) . . . . |

|

|

|

|

|

|

|

|

|

|

||||

22 |

Capital stock: |

a Preferred stock . . . . |

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

b Common stock . . . . |

|

|

|

|

|

|

|

|

|

|

||

23 |

Additional |

|

|

|

|

|

|

|

|

|

|

||||

24 |

Retained |

|

|

|

|

|

|

|

|

|

|

||||

25 |

Retained |

|

|

|

|

|

|

|

|

|

|

||||

26 |

Adjustments to shareholders’ equity (attach statement) |

|

|

|

|

|

|

|

|

|

|

||||

27 |

Less cost of treasury stock |

|

|

|

|

( |

) |

|

|

( |

) |

||||

28 |

Total liabilities and shareholders’ equity . . |

|

|

|

|

|

|

|

|

|

|||||

Schedule

Note: The corporation may be required to file Schedule

1 |

Net income (loss) per books |

7 |

Income recorded on books this year |

|

2 |

Federal income tax per books |

|

|

not included on this return (itemize): |

3 |

Excess of capital losses over capital gains . |

|

|

|

4Income subject to tax not recorded on books this year (itemize):

|

|

|

8 |

|

Deductions on this return not charged |

5 |

Expenses recorded on books this year not |

|

against book income this year (itemize): |

||

|

deducted on this return (itemize): |

a |

Depreciation . . $ |

||

a |

Depreciation . . . . $ |

b |

Charitable contributions $ |

||

bCharitable contributions . $

cTravel and entertainment . $

|

|

|

9 |

Add lines 7 and 8 |

6 |

Add lines 1 through 5 |

10 |

Income (page 1, line |

|

Schedule

1 |

Balance at beginning of year |

5 |

Distributions: a Cash |

||

2 |

Net income (loss) per books |

|

|

|

b Stock . . . . |

3 |

Other increases (itemize): |

|

|

|

c Property . . . . |

|

|

|

6 |

Other decreases (itemize): |

|

|

|

|

7 |

Add lines 5 and 6 |

|

4 |

Add lines 1, 2, and 3 |

8 |

Balance at end of year (line 4 less line 7) |

||

Form 1120 (2021)

Form Information

| Fact Name | Description |

|---|---|

| Purpose of Form 1120 | It's used by corporations to report their income, gains, losses, deductions, and credits, and to figure out their federal income tax liability. |

| Who Must File | Most U.S. corporations, including S corporations, must file Form 1120, unless they're exempt under section 501. |

| Due Date | The form is generally due by the 15th day of the 4th month following the end of the corporation's tax year. For corporations on a calendar year, this is April 15. |

| Extension Option | Corporations can apply for a six-month extension to file using Form 7004, which doesn't extend the time to pay any taxes owed. |

| Electronic Filing | Corporations can file this form electronically through the IRS e-file system, which is encouraged for faster processing and receipt confirmation. |

| State-Specific Versions | Some states require corporations to file a state-specific version of Form 1120 or a similar form, governed by the state's tax laws. |

Detailed Guide for Writing IRS 1120

Filling out the IRS Form 1120, which is used by corporations to report their income, gains, losses, deductions, credits, and to figure out their income tax liability, can seem daunting at first. However, breaking down the process into manageable steps can make it much more approachable. Ensuring accurate and complete information is crucial for compliance with tax laws and to avoid potential audits or penalties. The following steps are designed to guide you through the process of filling out the Form 1120 efficiently.

- Before beginning, gather all necessary documents, including the corporation's income statement, balance sheet, and records of dividends paid.

- Start by filling in the basic information about your corporation at the top of the form, including the legal name, address, date of incorporation, and EIN (Employer Identification Number).

- Enter the income details in the "Income" section. This includes gross receipts or sales, returns and allowances, cost of goods sold, and other forms of income. Subtract returns and allowances from gross receipts to find the gross income.

- Report deductions. The form includes spaces for salaries and wages, rent, taxes, and licenses, interest, and other deductions. Ensure you have documentation for all claims made in this section.

- Calculate the corporation’s taxable income by subtracting the total deductions from the total income.

- Apply any tax credits for which the corporation is eligible. This section can help reduce the total amount of tax the corporation owes.

- Fill out Schedule J to calculate the tax owed. This involves applying the appropriate tax rate to the taxable income calculated earlier.

- If applicable, complete Schedules K and L. Schedule K is for additional information on the corporation's financial state, and Schedule L is a balance sheet per books if required.

- Review the form thoroughly. Ensure all necessary sections are filled out and that the information provided is accurate to the best of your knowledge.

- Sign and date the form. An officer of the corporation must sign the form, affirming that the information is accurate and complete.

- Lastly, submit the form to the IRS by the filing deadline, which is typically April 15 for calendar year filers, or the 15th day of the fourth month after the end of your fiscal year if you file on a fiscal year basis. Consider electronic filing for quicker processing.

Completing the IRS Form 1120 requires careful attention to detail and an understanding of your corporation's financial activities throughout the tax year. By following these steps carefully, corporations can ensure they meet their obligations and provide the necessary information to the IRS in a structured and organized manner. Remember, when in doubt, consulting with a tax professional can provide additional clarity and help avoid potential issues.

Important Points on IRS 1120

What is the IRS 1120 form used for?

The IRS 1120 form, often referred to as the U.S. Corporation Income Tax Return, serves the purpose of reporting the income, gains, losses, deductions, and credits of a corporation. This form determines the income tax liability of a corporation, ensuring compliance with U.S. tax law. Unlike individual tax returns, the 1120 is specifically designed for corporate entities, contributing to organized federal tax administration.

Who is required to file an IRS 1120 form?

Generally, any corporation operating within the United States or receiving income from U.S. sources must file an IRS 1120 form. This includes corporations in all industries, with specific forms and schedules for certain types of businesses, such as life insurance companies and S Corporations, which file different versions of the 1120 form. It’s important for corporations to assess their status annually to determine their filing requirements.

When is the IRS 1120 form due?

The deadline for filing the IRS 1120 form typically falls on the 15th day of the fourth month following the end of the corporation's tax year. For corporations operating on a calendar year, this means the deadline is usually April 15th. However, if the due date lands on a weekend or legal holiday, the deadline is extended to the next business day. Corporations can request a six-month extension to file using Form 7004.

What information is needed to complete the IRS 1120 form?

To properly fill out the IRS 1120 form, corporations will need comprehensive financial information for the tax year, including total income, cost of goods sold, gross profit, dividends, interest, rents, royalties, and any other income. Additionally, detailed records of deductions—such as salaries and wages, repairs, rentals, taxes, interests, and depreciation—are necessary. Correctly calculating tax liability requires precise financial data and understanding of applicable deductions and credits.

How can a corporation file an IRS 1120 form?

Corporations have the option to file the IRS 1120 form electronically through the IRS e-file system or by mailing a paper form to the IRS. Electronic filing is encouraged as it is generally faster, more secure, and offers immediate confirmation of receipt. For those opting to file on paper, it is crucial to use the most current form and follow the IRS guidelines for where to file, as the appropriate address may vary depending on the location of the corporation.

Common mistakes

Completing the IRS Form 1120, the U.S. Corporation Income Tax Return, is a complex process that presents numerous pitfalls for taxpayers. One common mistake is the failure to report all income accurately. This could range from overlooking a minor source of revenue to incorrectly classifying income, leading to incorrect tax calculations. Transparency and thoroughness in reporting are crucial to avoid potential audits and penalties.

Another frequent oversight involves deductions. Taxpayers often either claim deductions not allowed for corporations or fail to claim deductions they are entitled to. This not only affects the bottom line of the corporation's taxable income but also reflects on the accuracy of the tax return. Proper understanding and application of the tax code related to deductions can significantly benefit a corporation.

Incorrectly classifying employees and contractors can lead to serious tax implications. The IRS pays close attention to this classification because it affects payroll tax obligations. Misclassification may result in the imposition of back taxes, penalties, and interest. Corporations must meticulously review the criteria set forth by the IRS to correctly identify the status of their workers.

Not keeping up with changes in tax laws and regulations is yet another mistake. Tax laws are subject to frequent changes, and what was accurate in a previous year's return might not apply in the current year. Corporations must stay informed about these changes to ensure compliance and optimize their tax positions.

Filing late or with incorrect payment can carry heavy penalties. The deadlines for submitting Form 1120 and any payments due are clearly outlined by the IRS. Missing these deadlines can result in unnecessary financial burdens in the form of late fees and interest charges, underlining the importance of punctuality in tax matters.

Inaccurately calculating tax credits is a mistake that can lead to missed opportunities for reducing tax liability. Many corporations fail to fully understand or apply the range of tax credits available to them. These credits, designed to encourage certain business activities, can offer significant financial benefits if applied correctly.

An error often seen is the improper representation of capital gains or losses. These transactions must be reported in a specific manner on Form 1120. Incorrect reporting can affect the corporate tax rate applied and potentially flag the return for review. Understanding the intricacies of reporting these transactions is critical for accurate tax calculation.

Failure to maintain adequate records is a critical mistake. The IRS may request supporting documentation for items reported on Form 1120. Without proper records, substantiating claims made on the tax return becomes challenging, possibly leading to adjustments by the IRS that could increase tax liability or trigger an audit.

Last but certainly not least, attempting to navigate the complexities of Form 1120 without professional assistance is a notable misstep for many corporations. The intricacies of corporate tax law and the nuances of applying those laws can easily lead to errors. Engaging a tax professional who understands the details of corporate taxation can prevent many of the mistakes outlined above, ensuring compliance and potentially saving the corporation from costly penalties and wasted time.

Documents used along the form

When companies prepare their federal tax return using the IRS 1120 form, also known as the U.S. Corporation Income Tax Return, several additional documents often need to be completed alongside it. These forms aid in providing a comprehensive view of the company's financial activities, tax deductions, credits, and income specifics for the year. Here's a list of forms and documents frequently used with the IRS 1120 form to ensure all necessary information is accurately and thoroughly reported.

- Schedule K-1 (Form 1065): This form reports the income, deductions, and credits of each partner in a partnership. It's used to ensure partners are correctly reporting their share of partnership financial activity on their individual tax returns.

- Schedule D (Form 1120): It's used by corporations to report the sale or exchange of capital assets not reported on another form or schedule. It helps calculate the capital gains or losses, affecting the company's taxable income.

- Form 1125-A: Companies use this form to detail the cost of goods sold. It's essential for businesses that manufacture products or purchase them for resale, providing a clear picture of gross profit.

- Form 1125-E: This form reports compensation of officers, detailing the amounts paid to its top officers which can impact the business's taxable income.

- Form 4797: Used for reporting the sale of business property, this form helps separate the gains and losses from ordinary business operations from those stemming from property transactions.

- Form 4562: Companies use this to report depreciation and amortization, detailing deductions for assets such as equipment, vehicles, and software. It helps businesses reduce taxable income by accounting for the wearing down of assets over time.

- Form 8825: This is used by partnerships and S corporations to report income and expenses from real estate. It functions similarly to Schedule E (Form 1040), but is for entities, showing the impact of real estate holdings on their tax obligations.

- Form 8941: Employers use this to calculate the credit for small employer health insurance premiums. It supports businesses in reducing their tax burden by providing health insurance to their employees.

- Form 5472: Required for corporations engaged in a U.S. trade or business that have reportable transactions with foreign or related parties, ensuring transparency in international dealings.

- Form 8865: For U.S. persons who are partners in foreign partnerships, this form is used to report the partnership's income, deductions, gains, and losses. It ensures U.S. taxation is applied to foreign business activities as appropriate.

These documents serve as tools for detailed financial reporting and compliance with tax regulations. When used in conjunction with the IRS 1120 form, they provide a full picture of the company's financial health and obligations, ensuring accurate income reporting and tax calculation. It’s important for businesses to familiarize themselves with these forms to ensure compliance with IRS requirements and to make the most of potential tax benefits.

Similar forms

The IRS 1040 form is quite similar to the IRS 1120 form as both are pivotal in the tax reporting and return filing processes in the United States. However, while the 1120 form is designed for corporations, the 1040 form is tailored for individual taxpayers. Both forms require detailed income statements and calculate the taxes owed or refund due, but they cater to different entities within the tax ecosystem. They embody the principle of tax responsibility, whether for an individual or a corporate entity.

Another document that shares similarities with the IRS 1120 form is the IRS 1120S form. This form is specifically utilized by S corporations for tax filing. The key similarity lies in their purpose: both are used to report income, losses, and dividends of corporations. However, the 1120S form is distinct in that it allows profits and losses to be passed through directly to the shareholders’ personal tax returns, thereby avoiding the double taxation typically associated with corporate income.

The IRS 1065 form also bears resemblance to the 1120 form but serves a different audience. The 1065 form is used by partnerships for income and loss reporting. Like the 1120, it elaborates on the entity's financial activities over the tax year. While corporations use the 1120 to determine their income tax liability, partnerships report income and losses via the 1065, with the income and loss then distributed among partners to be reported on their individual tax returns.

Form 990 is reminiscent of the IRS 1120 form but is specifically designed for nonprofit organizations. Nonprofits use Form 990 to provide the public with financial information and to maintain their tax-exempt status with the IRS. Both forms serve as a comprehensive disclosure of financial data, but they cater to fundamentally different types of organizations, each with unique tax responsibilities and privileges.

The Schedule C (Form 1040) shares parallels with the IRS 1120 in terms of purpose for reporting business income and expenses, albeit from a sole proprietorship perspective. While the 1120 form is intended for corporations, Schedule C attaches to the personal tax return of a sole proprietor, providing a detailed account of business profits and losses that impact the individual’s overall tax calculation.

Form 5472, while more specialized, is similar to the IRS 1120 in that it deals with financial disclosures related to international transactions. Used by companies engaged in transactions with foreign related parties, Form 5472 complements the 1120 by providing a detailed account of international dealings, ensuring transparency and compliance with U.S. tax laws for corporations with international ties.

The state corporate income tax returns, although varying by state, mirror the IRS 1120 form in purpose and substance. These state-specific forms require corporations to report their income, deductions, and credits to calculate the state tax liability. Similar to the federal 1120, they ensure corporations contribute their fair share to state tax revenues, adapted to each state's tax codes and rates.

Lastly, the Employment Tax Forms, like Form 941, resemble the IRS 1120 in that they are essential filings for entities with employees, but they focus on payroll taxes rather than income tax. While the 1120 accounts for a corporation's annual income tax liability, forms such as the 941 report on quarterly payroll taxes, including withheld income taxes and both the employee's and employer's share of social security and Medicare taxes.

Dos and Don'ts

Filing the IRS 1120 form, which is the U.S. Corporation Income Tax Return, requires careful attention to detail and adherence to specific procedures. Below are essential dos and don'ts to guide you through the process:

- Do gather all necessary documents beforehand, including income statements, balance sheets, and receipts for deductions and credits.

- Do use the correct form version for the tax year you are filing for, ensuring all information is relevant and up-to-date.

- Do double-check your calculations to prevent errors that could delay processing or prompt audits.

- Do utilize the IRS electronic filing system if possible, for a faster and more secure submission.

- Do sign and date the form, as an unsigned tax return is considered invalid.

- Don't leave any required fields blank. If a particular section does not apply, enter "0" or "N/A".

- Don't underestimate the importance of deadlines. Late filings can result in penalties and interest charges.

- Don't overlook the necessity to attach all required schedules and forms that relate to your tax situation.

- Don't hesitate to seek professional assistance if you're uncertain about any aspect of your tax return to ensure compliance and accuracy.

Misconceptions

When it comes to taxes, there's a lot of confusion out there, especially regarding the IRS Form 1120, which is used by corporations to report their income, gains, losses, deductions, and credits and to figure out their income tax liability. Let’s clear up some of the most common misunderstandings about this form.

Only large corporations need to file Form 1120. In truth, all corporations that are incorporated in the United States or that conduct business in the U.S. must file Form 1120, regardless of their size.

Form 1120 is due on April 15. Actually, the due date for Form 1120 can vary depending on the corporation's tax year. For those following a calendar year, the form is due on April 15. However, for corporations that operate on a fiscal year, the deadline is the 15th day of the fourth month following the end of their fiscal year.

S-corporations also file Form 1120. This is incorrect. S-corporations file Form 1120S, not 1120. The “S” designation is crucial, as it differentiates between the two forms and represents a different tax structure for small businesses that qualify.

If your corporation didn’t earn any income, you don’t need to file Form 1120. Even if your corporation didn't earn income, it's still required to file Form 1120. The IRS requires all corporations to file, regardless of income or activity levels during the year.

Filing Form 1120 automatically triggers an IRS audit. This is a myth. Filing Form 1120 does not automatically trigger an audit. Audits are selected based on a variety of criteria, including randomness, comparison of various data, and more, not merely the filing of any particular form.

You can file Form 1120 electronically yourself without any issue. While it is possible to e-file Form 1120, it's often recommended to seek the guidance of a tax professional due to the complexities involved in corporate taxation rules and regulations, which can be challenging to navigate without specialized knowledge.

Amendments to Form 1120 are not allowed. If you make a mistake on your original Form 1120, you can indeed file an amended return using Form 1120X. This rectifies any errors and ensures your corporation's tax responsibilities are accurate.

Form 1120 is only for reporting income. This form is utilized not just for reporting income but also for disclosing deductions, credits, and other relevant financial information about the corporation, providing a comprehensive view of its fiscal health and tax obligations.

Once you submit Form 1120, you cannot request an extension. Corporations can request an extension for filing Form 1120 by submitting Form 7004 before the original due date, granting them an additional six months to file.

Profit is taxed at a flat rate for all corporations. The Tax Cuts and Jobs Act of 2017 established a flat corporate income tax rate of 21%, but it’s a misconception that this is the only tax rate that applies to corporate profits. Other taxes and rates can apply, depending on various factors such as income amounts, deductions, and credits.

Understanding these misconceptions can help demystify some of the complexities surrounding corporate taxation and Form 1120, leading to more informed decisions and compliance with tax regulations.

Key takeaways

The IRS 1120 form, crucial for corporate tax filing, holds the potential to be overwhelming. Here are several key takeaways to guide taxpayers through this process smoothly, ensuring they meet their legal obligations while possibly maximizing their benefits.

- Understand the Purpose: The IRS 1120 form is specifically designed for corporations to report their income, gains, losses, deductions, and credits, along with calculating their federal income tax liability.

- Know Who Must File: Most C corporations and LLCs that have elected to be treated as corporations need to file Form 1120. This requirement applies whether the company has taxable income or not.

- Be Timely: Typically, Form 1120 must be filed by the 15th day of the fourth month following the end of the corporation's tax year. For those operating on a calendar year, the deadline is April 15. Extensions are available but must be filed by the original due date.

- Gather Required Information: Before starting the form, it’s essential to compile comprehensive financial records for the year, including income statements, balance sheets, and documents pertaining to deductions and credits.

- Understand Tax Rates: Corporate tax rates can vary, so it’s important to understand which rate applies to your company. This ensures the correct calculation of your tax liability.

- Consider State Requirements: In addition to federal taxes, most states require corporations to file a corresponding state income tax return. Ensure you are aware of and comply with the requirements in states where your corporation operates.

- Seek Expert Advice: The complexities of corporate tax can be daunting. Professional advice from a certified public accountant or a tax attorney can provide valuable guidance, helping to navigate the nuances of the tax code and potentially uncovering opportunities for savings.

Fulfilling corporate tax obligations accurately and on time is vital for any business. Understanding the importance and requirements of the IRS 1120 form is the first step in mastering corporate tax filings, ultimately contributing to a company’s compliance and financial health.

Discover Other PDFs

Pre Trip Inspection Class a Pdf With Pictures - Helps ensure the driver’s safety by identifying and addressing any vehicle vulnerabilities.

Abn Form Meaning - Patients have the option to contact Medicare directly for clarification or further information about coverage and ABNs.