Cg 20 10 07 04 Liability Endorsement Form

Navigating the realm of commercial general liability insurance can often seem like a complex journey, dotted with various policy changes and endorsements that tailor coverage to specific needs. Among these, the CG 20 10 07 04 Liability Endorsement form stands out as a crucial document for businesses, especially those involved in construction, leasing, or contracting. This particular form modifies the standard commercial general liability coverage to include additional insureds, namely owners, lessees, or contractors, under specific conditions. It ensures that these parties are covered for liability related to "bodily injury," "property damage," or "personal and advertising injury" that might arise from the insured's actions or the actions of those working on their behalf. However, the coverage has its limitations and exclusions, particularly concerning the scope of coverage and the timing of the incurred liability. Notably, it also addresses the insurance limits, specifying that coverage for additional insureds shall not exceed the requirements of a contract or the policy's limits, whichever is less. Understanding the nuances of the CG 20 10 07 04 can be instrumental for businesses looking to manage risks effectively in their operations and contractual engagements.

Sample - Cg 20 10 07 04 Liability Endorsement Form

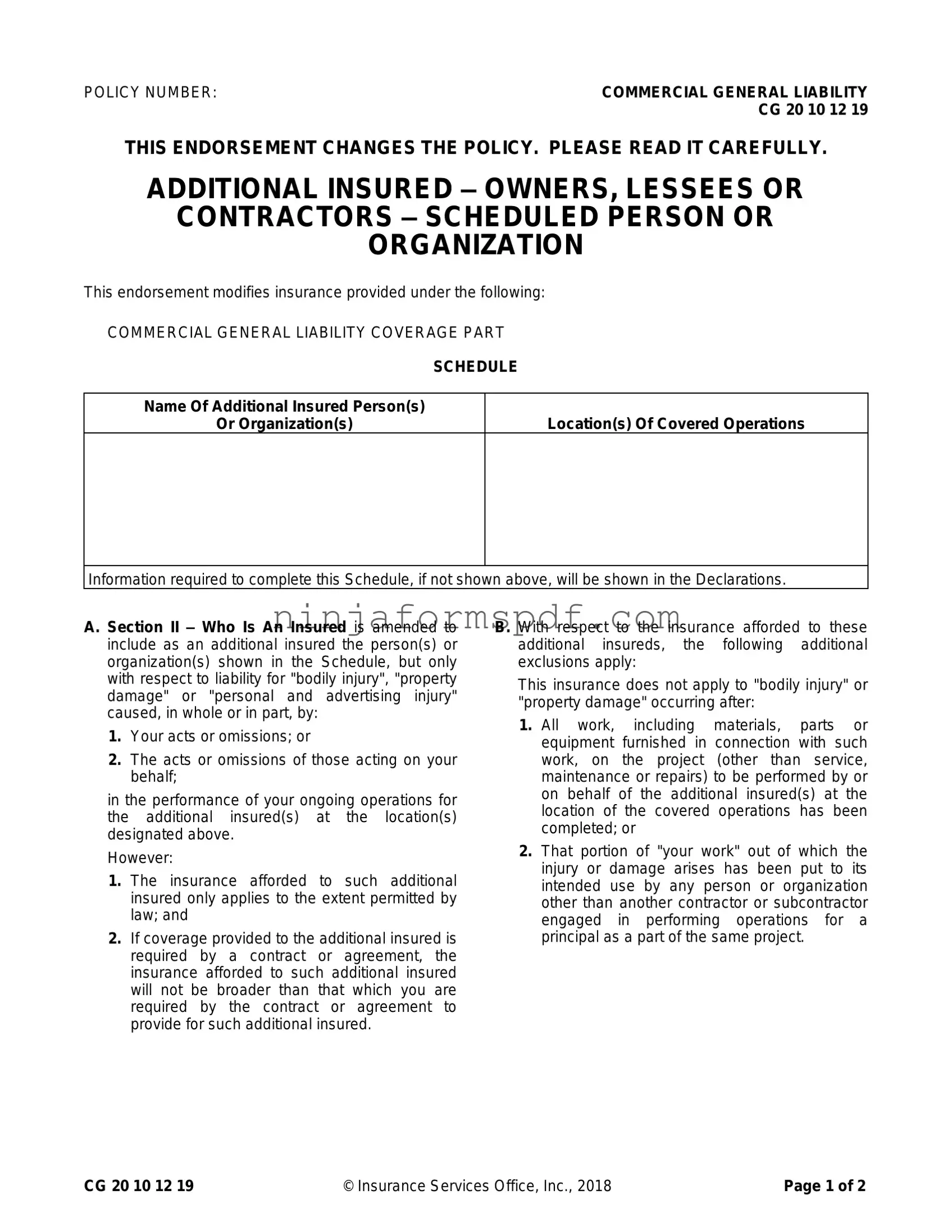

POLICY NUMBER: |

COMMERCIAL GENERAL LIABILITY |

|

CG 20 10 12 19 |

THIS ENDORSEMENT CHANGES THE POLICY. PLEASE READ IT CAREFULLY.

ADDITIONAL INSURED – OWNERS, LESSEES OR

CONTRACTORS – SCHEDULED PERSON OR

ORGANIZATION

This endorsement modifies insurance provided under the following:

COMMERCIAL GENERAL LIABILITY COVERAGE PART

SCHEDULE

Name Of Additional Insured Person(s)

Or Organization(s)

Location(s) Of Covered Operations

Information required to complete this Schedule, if not shown above, will be shown in the Declarations.

A. Section II – Who Is An Insured is amended to include as an additional insured the person(s) or organization(s) shown in the Schedule, but only with respect to liability for "bodily injury", "property damage" or "personal and advertising injury" caused, in whole or in part, by:

1.Your acts or omissions; or

2.The acts or omissions of those acting on your behalf;

in the performance of your ongoing operations for the additional insured(s) at the location(s) designated above.

However:

1.The insurance afforded to such additional insured only applies to the extent permitted by law; and

2.If coverage provided to the additional insured is required by a contract or agreement, the insurance afforded to such additional insured will not be broader than that which you are required by the contract or agreement to provide for such additional insured.

B. With respect to the insurance afforded to these additional insureds, the following additional exclusions apply:

This insurance does not apply to "bodily injury" or "property damage" occurring after:

1.All work, including materials, parts or equipment furnished in connection with such work, on the project (other than service, maintenance or repairs) to be performed by or on behalf of the additional insured(s) at the location of the covered operations has been completed; or

2.That portion of "your work" out of which the injury or damage arises has been put to its intended use by any person or organization other than another contractor or subcontractor engaged in performing operations for a principal as a part of the same project.

CG 20 10 12 19 |

© Insurance Services Office, Inc., 2018 |

Page 1 of 2 |

C. With respect to the insurance afforded to these additional insureds, the following is added to

Section III – Limits Of Insurance:

If coverage provided to the additional insured is required by a contract or agreement, the most we will pay on behalf of the additional insured is the amount of insurance:

1.Required by the contract or agreement; or

2.Available under the applicable limits of insurance;

whichever is less.

This endorsement shall not increase the applicable limits of insurance.

Page 2 of 2 |

© Insurance Services Office, Inc., 2018 |

CG 20 10 12 19 |

Form Information

| Fact Number | Description |

|---|---|

| 1 | The form identifier is CG 20 10 12 19. |

| 2 | This endorsement modifies the commercial general liability coverage. |

| 3 | It specifically relates to additional insured parties identified in the Schedule. |

| 4 | Coverage extends to liabilities arising from the insured's acts or omissions and those acting on their behalf. |

| 5 | Insurance coverage is contingent upon the extent permitted by law. |

| 6 | Limitations include that coverage will not exceed requirements of a contract or agreement to provide for an additional insured. |

| 7 | New exclusions for additional insureds are stated, particularly for injuries or damages occurring after completion of work or use of completed work. |

| 8 | For required coverage by contract or agreement, the maximum payable is the lesser of required amount or available limits. |

| 9 | This endorsement does not increase the overall limits of insurance. |

| 10 | The form is copyrighted by Insurance Services Office, Inc., 2018. |

Detailed Guide for Writing Cg 20 10 07 04 Liability Endorsement

Filling out the CG 20 10 07 04 Liability Endorsement form is a pivotal step in ensuring that additional insureds, such as owners, lessees, or contractors, are covered under a commercial general liability policy. This process involves accurately documenting the details of the additional insured parties and understanding the extent of the coverage provided. The form modifies the existing policy to include specific individuals or organizations, changing the original terms and broadening the scope of who is covered. Essentially, it's about adding layers of protection for entities that have a stake in your business operations. Here’s a simplified guide on completing this form:

- Start by locating the POLICY NUMBER at the top of the form. This should match the number on your existing commercial general liability policy documents.

- Under the SCHEDULE section, specify the Name Of Additional Insured Person(s) Or Organization(s). Here, you’ll list the entities that you are adding to your policy as additional insureds.

- Next, fill in the Location(s) Of Covered Operations. This is where you detail the physical locations where the coverage will apply, directly relating to where the additional insureds conduct their business or services in connection with your operations.

- Review Section A, noting the conditions under which the additional insureds are covered by your policy. This area requires no action but understanding its content is crucial. It outlines the liability coverage in relation to your acts or the acts of those working on your behalf.

- Pay attention to Section B for additional exclusions that apply to the insurance provided to these additional insureds. Again, this section requires no direct input but is important for understanding the limitations of the coverage extension.

- In Section C, note that if the coverage extended to the additional insured is mandated by a contract or agreement, the limits of this insurance will be the lesser of what is required by the contract or what your policy can provide. This section underscores the importance of aligning contract requirements with policy limits.

After completing these steps, thoroughly review the form to ensure all information is accurately entered. This form is a critical component of your commercial general liability policy as it directly impacts the scope of protection offered to third parties associated with your operations. By diligently completing and understanding each part, you safeguard not only your interests but also those of your business partners.

Important Points on Cg 20 10 07 04 Liability Endorsement

What is the CG 20 10 07 04 Liability Endorsement form?

The CG 20 10 07 04 Liability Endorsement form is a document used in commercial general liability (CGL) insurance policies. It serves to add a person or organization as an additional insured under the policy. This is typically requested when a business enters into a contract that requires them to provide liability coverage for another party (such as a contractor, lessee, or owner). The form specifies conditions under which the additional insured is covered, particularly focusing on liability arising from the named insured's operations or premises.

Who needs to be listed as an additional insured?

Entities or individuals who have a contractual requirement or a vested interest in being protected under your liability policy should be listed as additional insureds. This often includes owners, lessees, or contractors involved in your business operations. Essentially, if someone's actions on behalf of your business could expose them to legal liability, or if a contract stipulates it, they should be added via a form like CG 20 10 07 04 to your insurance policy.

How does adding an additional insured affect my insurance policy?

Adding an additional insured to your policy extends your coverage to protect the additional insured against claims arising from your operations or premises. This does not generally increase your premium, depending on the specifics of the insurance agreement. However, it’s important to note that the policy limits are shared with the additional insured, meaning any claim paid out also reduces the limit available for your own claims under the same policy.

Are there limitations to the coverage for an additional insured?

Yes, there are specific limitations. The CG 20 10 07 04 form outlines that coverage for additional insureds is "caused, in whole or in part, by: 1. Your acts or omissions; or 2. The acts or omissions of those acting on your behalf." Furthermore, the coverage also adheres to legal requirements and contractual obligations, and it won't cover any events happening after the completion of the work. It's also limited by the insurance policy's terms, conditions, and exclusions.

What happens if the coverage required by a contract exceeds my policy limits?

When coverage required by a contract exceeds your policy limits, the insurance provided to the additional insured will only extend up to the limits of your current policy, unless otherwise stipulated in your insurance agreement. The form specifically states that coverage for additional insureds required by contract will not exceed the lesser of the contract requirements or the policy's limits. If the required limits are higher than your policy allows, you may need to adjust your policy or purchase additional coverage to comply with contractual obligations.

Common mistakes

Filling out the CG 20 10 07 04 Liability Endorsement form involves providing accurate details about additional insured entities under a commercial general liability policy. However, individuals often make mistakes that can lead to issues down the line. Understanding these common errors is the first step towards avoiding potential complications.

One of the most frequent mistakes is not specifying the full legal name of the additional insured. It is crucial to use the name as it appears in legal documents to ensure the correct entity is covered. Abbreviations or nicknames may lead to confusion and inadequate coverage.

An equally significant oversight is failing to accurately describe the location(s) of covered operations. This section must detail where the covered activities will occur, and any inaccuracies or omissions can result in disputes over whether a claim falls within the policy's scope. Precise descriptions set clear boundaries for coverage.

There's also a tendency to overlook the necessity of aligning the coverage with the requirements of a contract or agreement. When the form states that coverage for an additional insured will not exceed what is contractually mandated, neglecting to verify that the policy meets these stipulations can lead to insufficient protection for the additional insured.

Additionally, misunderstanding the limitations regarding the timeframe of coverage can be problematic. The form clearly indicates that coverage for additional insureds does not apply to damages or injuries occurring after the completion of work or after the completed work has been put to its intended use. Misinterpreting these temporal limits may lead to false assumptions about the duration of coverage.

Another error involves misreading the provisions that cap the amount payable on behalf of an additional insured to either the amount required by contract/agreement or the policy limit, whichever is lower. Ignoring these caps can result in unrealistic expectations about the policy's payout in the event of a claim.

Often, there is a lack of review regarding the additional exclusions applicable to additional insureds. Each policy may have unique exclusions that significantly affect the scope of coverage. Overlooking these can leave the additional insured unaware of the gaps in their protection.

The form's requirement that it does not increase the limits of insurance for the policy as a whole is another area of misunderstanding. This means that any claims paid on behalf of an additional insured count towards the policy's overall limits. Misapprehensions about how this affects the total available coverage can lead to unwanted surprises during claims.

A crucial but often neglected part of filling out this form is not ensuring consistent information across all related documents. Discrepancies between the form and other policy documents or contracts can lead to challenges in enforcing the terms of the coverage.

Finally, the failure to update the form when there are changes in the underlying contractual requirements or in the scope of the ongoing operations can result in outdated information that jeopardizes coverage. Regular reviews and updates are necessary to maintain the relevance and accuracy of the information provided.

By being attentive to these common pitfalls, those filling out the CG 20 10 07 04 form can better ensure that the coverage provided matches the needs and expectations of all parties involved. Careful completion of this form is instrumental in securing the intended liability protection for additional insureds.

Documents used along the form

When handling insurance, especially in the realm of commercial general liability, the CG 20 10 07 04 Liability Endorsement is a critical document. It extends coverage to additional insureds, typically for businesses engaging in partnerships, leasing, or contracting work. This document ensures that certain individuals or organizations are covered under the policy, specifically for liabilities arising from the policyholder's operations connected to them. While this endorsement plays a significant role in managing risk and compliance, it often requires the support of additional forms and documents to provide a comprehensive insurance solution. The following are some of these essential documents:

- Certificate of Insurance (COI): It serves as proof of insurance, summarizing the key aspects of a policy, including the types of coverage, policy limits, and effective dates. It's frequently requested by third parties wanting to verify insurance coverage before entering into contracts.

- Policy Declarations Page: This document outlines the specifics of the insurance coverage, including the named insured, policy period, coverage limits, and premiums. It essentially summarizes the policy agreements.

- Additional Insured Endorsement: Apart from the CG 20 10, there are various forms of additional insured endorsements that specify the scope of coverage extensions to additional insureds, tailoring coverage to specific needs and agreements.

- General Liability Policy: The foundational document of coverage, detailing the broad scope of protection provided against liability claims for bodily injury, property damage, and advertising injury, among others.

- Amendatory Endorsements: These documents modify the terms or coverage of the primary policy, adding, deleting, or altering the standard coverage to fit unique requirements.

- Exclusions Document: It lists all the coverage exclusions, clarifying what is not covered by the policy. This is crucial for understanding the limitations of the insurance coverage.

- Named Insured Endorsement: Specifies who is covered as a named insured under the policy, potentially including entities or individuals not automatically covered under standard definitions.

- Waiver of Subrogation: This provision prevents the insurer from seeking compensation from a third party that may have contributed to the loss. It’s often required in contracts where the parties agree to limit their right to recover damages from one another.

Together with the CG 20 10 07 04 Liability Endorsement, these documents form a network of legal and financial protections catering to the dynamic needs of businesses in diverse industries. Proper management and understanding of these documents facilitate smoother operations, help in mitigating risks, and ensure compliance with contractual obligations. Whether for a small project or a large-scale operation, these documents play a pivotal role in the scaffolding of commercial insurance.

Similar forms

The CG 20 33 – Additional Insured – Owners, Lessees or Contractors – Automatic Status When Required in Written Construction Agreement endorsement shares a core similarity with the CG 20 10 regarding its function to extend additional insured status. Both documents serve to amend a commercial general liability policy to include as additional insured entities such as owners, lessees, or contractors in relation to construction projects. The CG 20 33, however, automatically grants this status when a written agreement or contract mandates such coverage, potentially simplifying the process and broadening the scope under which additional insured status is provided without the need for individual endorsements to be listed per project or agreement.

The CG 24 26 – Amendment of Insured Contract Definition endorsement is akin to the CG 20 10 in that both play significant roles in delineating the scope of coverage under a commercial general liability policy. While the CG 20 10 focuses on expanding who is covered, specifically additional insureds, based on their relationship to the named insured's operations at specified locations, the CG 24 26 aims at refining what constitutes an insured contract. This can directly influence the breadth of coverage provided to the additional insureds, especially regarding liabilities arising from contracts categorized as insured contracts.

Another related document, the CG 00 01 – Commercial General Liability Coverage Form, serves as the foundational contract to which the CG 20 10 endorsement is attached. This coverage form outlines the primary provisions, including coverage limits, exclusions, and the insuring agreement, establishing the general liability insurance framework. The CG 20 10’s modifications, specifying conditions under which additional insureds are covered, operate within the parameters defined by the CG 00 01. Its alterations to who is an insured directly impact the coverage landscape sketched out by the CG 00 01.

The CG 21 39 – Contractual Liability Limitation endorsement parallels the CG 20 10 in its effect on the scope of liability coverage, albeit in a restrictively modifying manner. Whereas the CG 20 10 extends coverage to additional insureds for liabilities arising from the named insured’s activities, the CG 21 39 limits coverage by excluding certain contractual liabilities from the policy’s ambit. This endorsement exemplifies a counterpoint to the CG 20 10’s expansive approach, emphasizing the careful balance insurers maintain between extending and restricting coverage through endorsements to suit various risk management needs.

Dos and Don'ts

When filling out the CG 20 10 07 04 Liability Endorsement form, it’s important to navigate the process with accuracy and attention to detail. Here’s a list of do’s and don'ts that can guide you through completing the form correctly and ensuring that the additional insureds are properly covered.

- Do thoroughly read the entire form before starting to fill it out. Understanding the scope and changes it brings to the policy helps in filling it out accurately.

- Do accurately list the name(s) of the additional insured person(s) or organization(s) in the Schedule section. This is crucial for the correct application of coverage.

- Do specify the exact location(s) of covered operations clearly. This detail is essential for the insurer to understand where the coverage applies.

- Do check the limits of insurance required by any contract or agreement mentioned, ensuring that they align with what you declare on the form.

- Do be aware of the exclusions and limitations regarding the additional insureds, mentioned in the endorsement, to manage expectations and coverage scope accurately.

- Don't assume that adding someone as an additional insured extends all your policy benefits to them. The coverage is modified as per the endorsement's terms.

- Don't overlook the importance of consulting with a legal or insurance professional if there are any confusions or uncertainties. Mistakes could lead to significant gaps in coverage.

By adhering to these do’s and don'ts, the process of completing the CG 20 10 07 04 Liability Endorsement form becomes more straightforward and ensures that the additional insureds are properly covered according to the policy terms and any related agreements.

Misconceptions

Understanding the CG 20 10 07 04 Liability Endorsement form can often be complex, leading to a number of misconceptions. Below, some common misunderstandings are clarified to provide a clearer picture of what this endorsement entails.

Misconception #1: It covers all types of liability. The form specifically provides coverage for "bodily injury", "property damage", or "personal and advertising injury" that occur due to the insured's actions or those acting on their behalf. It doesn't cover all types of liability.

Misconception #2: Additional insureds are covered for all their activities. Coverage is only extended to the additional insureds with respect to liability directly connected to the insured’s operations performed for them at the designated locations.

Misconception #3: The coverage is unlimited. If the additional insured coverage is required by a contract, the extent of the coverage will not surpass what is mandated by that contract, nor will it exceed the limits specified in the policy.

Misconception #4: It provides ongoing coverage after work completion. The endorsement excludes coverage for injuries or damages occurring after the insured's work has been completed or put to its intended use.

Misconception #5: The endorsement applies retroactively. The coverage applies only from the endorsement's effective date onwards and does not retroactively cover previous incidents or claims.

Misconception #6: It automatically extends the policy limits. The endorsement specifies that it does not increase the policy's existing limits of insurance. The coverage provided to an additional insured will not exceed the contracted requirements or the policy's limits, whichever is lesser.

Misconception #7: All additional insureds have the same coverage. Coverage is tailored to the specifics of the contract or agreement and the operations performed. It may vary significantly between additional insureds based on the nature of their relationship with the named insured and the scope of work.

It’s critical for all parties involved to thoroughly review and understand the specifics of the CG 20 10 07 04 Liability Endorsement to ensure that coverage aligns with expectations and requirements. Misconceptions can lead to unexpected coverage gaps and disputes in the event of a claim.

Key takeaways

Filling out and using the CG 20 10 07 04 Liability Endorsement form accurately is crucial for ensuring the right coverage and compliance with insurance policies. Here are key takeaways to consider:

- The form extends commercial general liability coverage to additional insured persons or organizations, primarily in scenarios where operations are performed on their behalf, which might result in bodily injury, property damage, or personal and advertising injury.

- It is essential to provide precise details in the Schedule about the additional insured person(s) or organization(s) and the location(s) of the covered operations to ensure that the endorsement is correctly attributed and effective.

- Coverage under this endorsement is contingent upon the acts or omissions of the named insured or those acting on their behalf. It specifically looks at the operations performed for the additional insured(s) at the designated locations.

- There are built-in limitations and exclusions to the coverage offered. For instance, once the work is completed or the part of the work out of which injury or damage arises is used by someone other than another contractor or subcontractor involved in the project, the insurance ceases to apply to related bodily injury or property damage.

- The coverage amount for additional insureds might be limited to what is required by a contract or agreement or to the available limits of insurance, whichever is less. Importantly, this endorsement does not increase the overall limits of insurance provided by the policy.

Understanding these aspects of the CG 20 10 07 04 form ensures that all parties are appropriately covered and aware of the scope and limits of the insurance protection provided.

Discover Other PDFs

How to Get Your Marriage Certificate - Often used in legal settings to prove a spouse's eligibility for benefits.

Shared Well Agreement Template - Offers peace of mind by clearly laying out each party's rights and responsibilities in relation to the shared water supply.