Broker Price Opinion Form

When it comes to real estate transactions, having a clear understanding of a property's value is crucial for lenders, agents, and potential buyers. Enter the Broker Price Opinion (BPO) form, a document designed to provide a comprehensive valuation of residential property. This form captures an array of vital data, including general market conditions indicating if the market is depressed, stable, or improving, alongside employment trends. Moreover, it delves into the specifics of the property in question, addressing its marketability, comparing it with other properties in the area, and evaluating its condition and the necessary repairs to make it market ready. The BPO also explores competitive listings to offer a precise market value, suggesting listing prices both in its current state and after repairs. This evaluation isn't just a number—it's an in-depth analysis covering everything from neighborhood occupancy rates to the potential reasons a property hasn't sold previously, providing key insights into not just the value but also the saleability of a property.

Sample - Broker Price Opinion Form

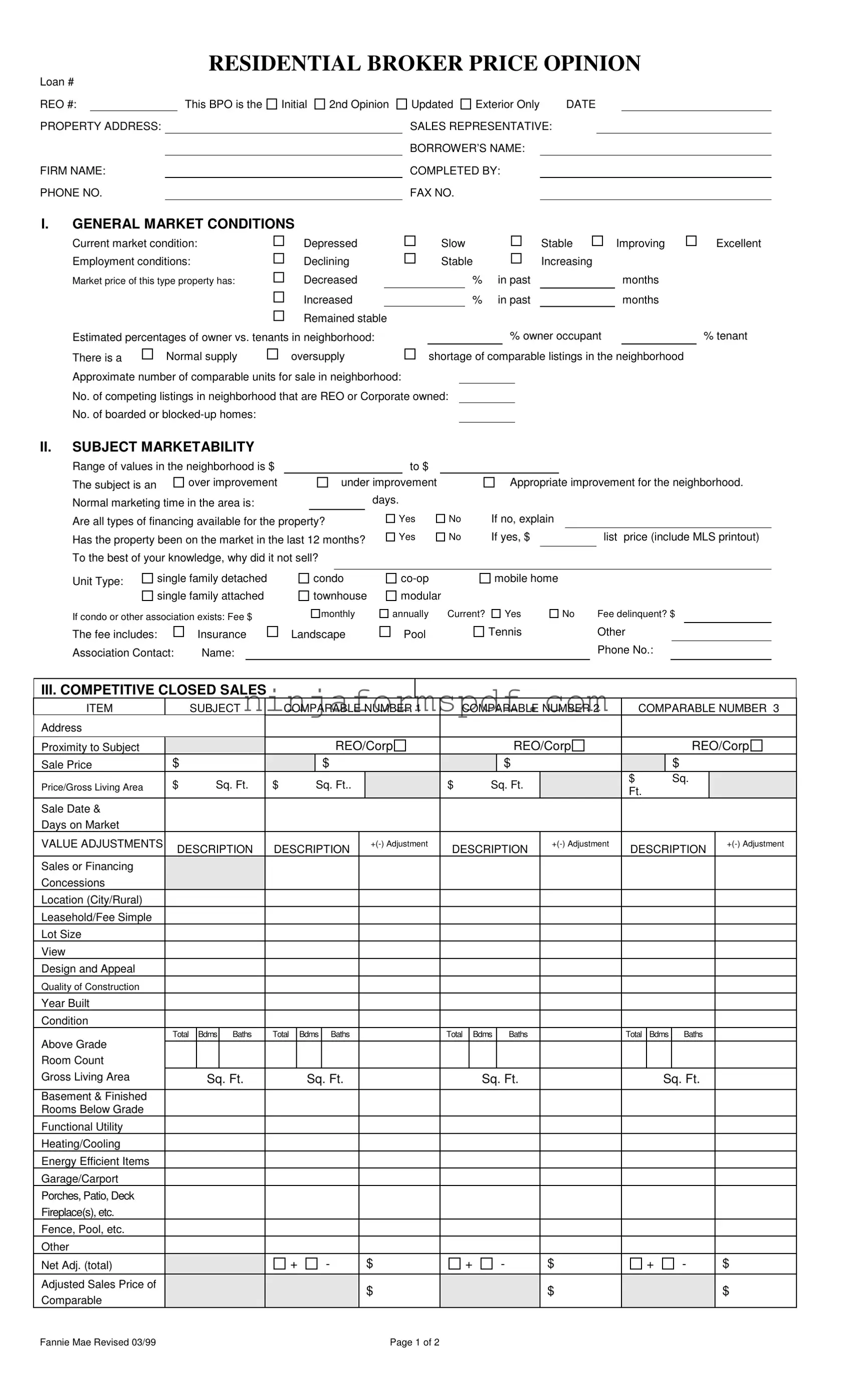

RESIDENTIAL BROKER PRICE OPINION

Loan #

REO #:This BPO is the

PROPERTY ADDRESS:

FIRM NAME:

PHONE NO.

Initial

2nd Opinion

Updated Exterior Only |

DATE |

|||

SALES REPRESENTATIVE: |

|

|

|

|

BORROWER’S NAME: |

|

|

|

|

COMPLETED BY: |

|

|

|

|

FAX NO. |

|

|

|

|

I.GENERAL MARKET CONDITIONS

Current market condition: |

Depressed |

Slow |

|

Stable |

Improving |

||

Employment conditions: |

Declining |

Stable |

|

Increasing |

|

||

Market price of this type property has: |

Decreased |

|

|

% |

in past |

|

months |

|

Increased |

|

|

% |

in past |

|

months |

|

Remained stable |

|

|

|

|

|

|

Estimated percentages of owner vs. tenants in neighborhood: |

|

|

% owner occupant |

|

|||

There is a |

Normal supply |

oversupply |

shortage of comparable listings in the neighborhood |

||||

Approximate number of comparable units for sale in neighborhood: |

|

|

|

|

|

||

No. of competing listings in neighborhood that are REO or Corporate owned:

No. of boarded or

Excellent

% tenant

II.SUBJECT MARKETABILITY

Range of values in the neighborhood is $ |

|

|

|

|

|

to $ |

|

|

|

|

|

|

|

|

The subject is an |

over improvement |

|

|

under improvement |

|

Appropriate improvement for the neighborhood. |

||||||||

Normal marketing time in the area is: |

|

|

|

|

days. |

|

|

|

|

|

|

|||

Are all types of financing available for the property? |

Yes |

No |

If no, explain |

|

|

|

||||||||

Has the property been on the market in the last 12 months? |

Yes |

No |

If yes, $ |

|

|

list price (include MLS printout) |

||||||||

To the best of your knowledge, why did it not sell? |

|

|

|

|

|

|

|

|

|

|||||

|

|

|

|

|

|

|

|

|

|

|

||||

Unit Type: |

single family detached |

|

condo |

|

mobile home |

|

|

|

||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

single family attached |

|

townhouse |

modular |

|

|

|

|

|

|

||||

If condo or other association exists: Fee $

monthly

annually Current?

Yes

No |

Fee delinquent? $ |

The fee includes:

Association Contact:

Insurance

Name:

Landscape

Pool

Tennis |

Other |

|

Phone No.: |

III. COMPETITIVE CLOSED SALES

ITEM |

|

|

SUBJECT |

|

COMPARABLE NUMBER 1 |

|

COMPARABLE NUMBER 2 |

|

COMPARABLE NUMBER 3 |

|||||||||||||||||||||||

Address |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Proximity to Subject |

|

|

|

|

|

|

|

|

|

|

REO/Corp |

|

|

|

|

|

|

REO/Corp |

|

|

|

|

|

REO/Corp |

||||||||

Sale Price |

$ |

|

|

|

|

|

|

$ |

|

|

|

|

|

|

|

|

|

$ |

|

|

|

|

|

|

|

$ |

|

|

|

|||

Price/Gross Living Area |

$ |

|

Sq. Ft. |

$ |

|

Sq. Ft.. |

|

|

$ |

|

|

Sq. Ft. |

|

|

$ |

|

|

|

Sq. |

|

|

|

||||||||||

|

|

|

|

|

|

|

|

|

Ft. |

|

|

|

|

|||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

Sale Date & |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Days on Market |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

VALUE ADJUSTMENTS |

|

DESCRIPTION |

|

DESCRIPTION |

|

|

DESCRIPTION |

|

DESCRIPTION |

|

||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||||||||

Sales or Financing |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Concessions |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Location (City/Rural) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Leasehold/Fee Simple |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Lot Size |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

View |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Design and Appeal |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Quality of Construction |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Year Built |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Condition |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Total |

|

Bdms |

Baths |

|

Total |

Bdms |

|

Baths |

|

|

|

Total |

|

Bdms |

|

Baths |

|

|

Total |

Bdms |

Baths |

|

|

|

||||||

Above Grade |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Room Count |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Gross Living Area |

|

|

|

Sq. Ft. |

|

|

Sq. Ft. |

|

|

|

|

|

|

Sq. Ft. |

|

|

|

|

|

Sq. Ft. |

|

|

|

|||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Basement & Finished |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Rooms Below Grade |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Functional Utility |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Heating/Cooling |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Energy Efficient Items |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Garage/Carport |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Porches, Patio, Deck |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Fireplace(s), etc. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Fence, Pool, etc. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Other |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Net Adj. (total) |

|

|

|

|

|

+ |

- |

|

|

$ |

|

+ |

- |

|

$ |

|

+ |

|

|

- |

|

$ |

|

|||||||||

Adjusted Sales Price of |

|

|

|

|

|

|

|

|

|

|

|

|

$ |

|

|

|

|

|

|

|

|

$ |

|

|

|

|

|

|

|

|

$ |

|

Comparable |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Fannie Mae Revised 03/99 |

|

|

|

|

|

|

|

|

|

|

|

|

Page 1 of 2 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

REO# |

Loan # |

IV. MARKETING STRATEGY

Minimal Lender Required Repairs |

V. REPAIRS

Occupancy Status: Occupied

Repaired Most Likely Buyer:

Vacant

Unknown

Unknown

Owner occupant

Investor

Investor

Itemize ALL repairs needed to bring property from its present “as is” condition to average marketable condition for the neighborhood. Check those repairs you recommend that we perform for most successful marketing of the property.

$

$

$

$

$

$

$

$

$

$

|

|

|

|

GRAND TOTAL FOR ALL REPAIRS $ |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

VI. COMPETITIVE LISTINGS |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

ITEM |

|

|

SUBJECT |

COMPARABLE NUMBER 1 |

COMPARABLE NUMBER. 2 |

COMPARABLE NUMBER. 3 |

|||||||||||||||||||||

Address |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Proximity to Subject |

|

|

|

|

|

REO/Corp |

|

|

|

|

|

REO/Corp |

|

|

REO/Corp |

||||||||||||

List Price |

$ |

|

|

|

|

|

|

$ |

|

|

|

|

|

|

|

$ |

|

|

|

|

|

|

$ |

|

|

||

Price/Gross Living Area |

$ |

|

Sq.Ft. |

$ |

Sq.Ft. |

|

|

|

$ |

Sq.Ft. |

|

|

|

$ |

Sq.Ft. |

|

|

||||||||||

Data and/or |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Verification Sources |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

VALUE ADJUSTMENTS |

|

DESCRIPTION |

DESCRIPTION |

|

+ |

DESCRIPTION |

|

DESCRIPTION |

|||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Sales or Financing |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Concessions |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Days on Market and |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Date on Market |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Location (City/Rural) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Leasehold/Fee |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Simple |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Lot Size |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

View |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Design and Appeal |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Quality of Construction |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Year Built |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Condition |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Above Grade |

Total |

Bdms |

Baths |

Total |

Bdms |

Baths |

|

|

|

Total |

Bdms |

|

Baths |

|

Total |

Bdms |

|

Baths |

|

|

|||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Room Count |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Gross Living Area |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

|

Sq. Ft. |

|

Sq. Ft. |

|

|

|

Sq. Ft. |

|

|

|

Sq. Ft. |

|

|

|||||||||||||

Basement & Finished |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Rooms Below Grade |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Functional Utility |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Heating/Cooling |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Energy Efficient Items |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Garage/Carport |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Porches, Patio, Deck |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Fireplace(s), etc. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Fence, Pool, etc. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Other |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

Net Adj. (total) |

|

|

|

|

+ |

- |

|

|

|

$ |

|

|

+ |

- |

- |

|

$ |

|

|

+ |

- |

|

$ |

|

|

||

Adjusted Sales Price |

|

|

|

|

|

|

|

|

|

$ |

|

|

|

|

|

|

|

$ |

|

|

|

|

|

|

$ |

|

|

of Comparable |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

VI. THE MARKET VALUE (The value must fall within the indicated value of the Competitive Closed Sales).

Market Value |

Suggested List Price |

AS IS REPAIRED

30 Quick Sale Value

Last Sale of Subject, Price |

Date |

COMMENTS (Include specific positives/negatives, special concerns, encroachments, easements, water rights, environmental concerns, flood zones, etc. Attach addendum if additional space is needed.)

Signature: |

|

Date: |

Fannie Mae Revised 03/99 |

Page 2 of 2 |

CMS Publishing Company 1 800 |

Form Information

| Fact Name | Description |

|---|---|

| Purpose of the Form | This form is used to provide an opinion on the price of a residential property by a broker, indicating whether the market conditions favor the buying or selling of properties. |

| Sections Covered | It includes general market conditions, subject marketability, competitive closed sales, marketing strategy, repairs needed, competitive listings, and the determination of market value. |

| Types of Properties Evaluated | The form is versatile, covering a range of property types including single-family homes, condos, co-ops, mobile homes, townhouses, and modular homes. |

| Governing Law(s) | While not specified in the provided content, Broker Price Opinion forms are generally subject to both federal and state-specific real estate laws and regulations. |

Detailed Guide for Writing Broker Price Opinion

Filling out a Broker Price Opinion (BPO) form requires attention to detail and a comprehensive understanding of the property in question, as well as the current market conditions. This document plays a critical role in the real estate industry by helping to determine the possible selling price or value of a property. To ensure accurate and effective completion of a BPO, one must methodically work through each section, providing detailed and precise information. Follow the steps below to fill out the form correctly.

- Start by entering the Loan # and REO # at the top of the form, if applicable.

- Indicate whether the BPO is an Initial, 2nd Opinion, Updated, or Exterior Only assessment.

- Fill in the PROPERTY ADDRESS, FIRM NAME, and PHONE NO.

- Enter the date and the SALES REPRESENTATIVE, BORROWER’S NAME, and the person COMPLETED BY along with the FAX NO.

- In the section titled GENERAL MARKET CONDITIONS, describe the current market by selecting the appropriate conditions and filling in the percentages or descriptions as requested.

- Under SUBJECT MARKETABILITY, indicate the range of values, subject's marketability compared to the neighborhood, and other specifics like financing availability, and if the property has been on the market in the last 12 months.

- For COMPETITIVE CLOSED SALES, list down details of the subject property and compare it with up to three comparable sales, including address, proximity to subject, and sales details.

- Fill out the VALUE ADJUSTMENTS section by describing and making necessary adjustments in value based on various factors for each comparable sale.

- In the MARKETING STRATEGY section, check the condition of the property and the required repairs, and describe the most likely buyer.

- List all repairs needed in the REPAIRS section with costs to bring the property to marketable condition.

- In COMPETITIVE LISTINGS, detail comparable active listings, noting their address, list price, and other pertinent attributes for comparison.

- Under THE MARKET VALUE, provide your calculated market value, suggest a list price for both as-is and repaired conditions, and indicate a quick sale value.

- In the COMMENTS section, note any positives, negatives, or special concerns about the property that could affect its value, including legal or environmental concerns. Attach an addendum if more space is needed.

- Finally, sign and date the form at the bottom to certify your assessment.

Upon completing the form, ensure all information is reviewed for accuracy. This document will be used in the decision-making process regarding the property, so it's important that it reflects a fair and unbiased valuation based on current market conditions and the specifics of the property itself. Follow up may involve discussions with financial institutions, real estate professionals, or potential buyers based on the findings in this report.

Important Points on Broker Price Opinion

What is a Broker Price Opinion (BPO)?

A Broker Price Opinion (BPO) is an assessment conducted by a real estate broker to estimate the value of a property. It examines various factors including market conditions, the property's condition, and comparable sales in the neighborhood to provide a suggested selling price or value.

When is a BPO used instead of a full appraisal?

BPOs are often used in situations where a quick, less expensive alternative to a full appraisal is needed. This includes scenarios such as a mortgage company evaluating a home for a loan modification, for short sales, or for foreclosures (REO properties). They're not as detailed as full appraisals but provide sufficient information for these purposes.

What information does a BPO contain?

A BPO report includes data on current market conditions, employment conditions, neighborhood occupancy rates, listing information about comparable sales, and any necessary repairs to bring the property up to marketable condition. Additionally, it provides a market value estimate and suggested list price for the property in its current and repaired state.

How are the market conditions assessed in a BPO?

Market conditions are evaluated based on the current economic climate, including whether the market is depressed, slow, stable, or improving. Factors such as employment conditions, percentage change in property prices, and the supply-demand balance in the neighborhood also play a critical role in this assessment.

Can a BPO suggest repairs for the property?

Yes, a section of the BPO is dedicated to identifying and itemizing necessary repairs to elevate the property to an average marketable condition. It even specifies which repairs are recommended for successful marketing of the property, along with the estimated costs for these repairs.

How does a BPO determine the property's market value?

The market value in a BPO is determined by analyzing comparable closed sales within the neighborhood, adjustments made for specific property features or conditions, and competitive listings. The final market value must align with the indicated value range derived from these comparisons.

What is the significance of "Current market condition" in a BPO?

The "Current market condition" section provides a snapshot of the economic environment affecting property sales. It indicates whether prices are trending up or down and gives insights into the speed and direction of the market, which significantly impacts the estimation of a property’s value.

What does "Occupancy Status" indicate in a BPO?

"Occupancy Status" reveals whether the property is currently occupied, vacant, or if the status is unknown. This information is crucial as it can affect the property's marketability, value, and the strategy recommended for selling or repairing the property.

Common mistakes

Filling out the Broker Price Opinion (BPO) form demands attention to detail and an in-depth understanding of market conditions, property status, and reporting accuracy. A common mistake is an incorrect evaluation of current market conditions, including misjudging the employment conditions and market trends for the type of property in question. This misinterpretation may lead to a skewed perspective on the property’s true market value.

Another area where errors frequently occur is in the determination of subject marketability. Incorrectly categorizing a property as an over or under improvement for the neighborhood can significantly impact the property evaluation. Additionally, inaccuracies in reporting previous market exposure—including failing to provide details of prior listings and reasons for not selling—can mislead the valuation process.

When it comes to competitive closed sales, a common error is not accurately adjusting for differences between the subject property and comparables. This section requires careful analysis of factors such as location, property condition, and amenities. Overlooking or improperly adjusting for these factors can lead to inaccurate valuation, affecting the reliability of the BPO.

Market strategy and recommended repairs are areas often mishandled in the form. Underestimating or overestimating repair costs, or failing to accurately identify the most likely buyer, can lead to misguided marketing strategies that don’t align with maximizing the property's value or appeal.

Listing competitive properties without thorough research on their list price and characteristics can result in an inaccurate competitive market analysis. Not updating or verifying the current status of comparable listings, such as changes in list prices or removal from the market, is a critical oversight.

Incorrectly estimating the value adjustments based on differences in sales or financing concessions, days on the market, and property specifics like lot size or view, can misrepresent the property’s market position. Being too generic or overlooking minor details in this section diminishes the form's effectiveness in capturing the true essence of the property’s value.

Not fully exploring marketing strategies that align with the property’s condition or potential buyer demographics can also misguide the decision-making process. The choice between as-is sales, minimal repairs, or lender-required repairs needs careful consideration to optimize property appeal and value.

Another frequent error is failing to provide detailed comments on specific positives/negatives, special concerns, and additional factors such as environmental concerns or easements that might impact the property’s value. This omission can lead to critical value influencers being overlooked.

Lastly, a lack of comprehensive review before submission leads to various errors across the form. This negligence may result in overlooking or misstating crucial details that affect the overall accuracy and credibility of the BPO.

Documents used along the form

In the real estate and mortgage industry, alongside the Broker Price Opinion (BPO) form, a variety of supporting documents and forms play crucial roles in the evaluation, acquisition, and sale of properties. These documents ensure a comprehensive approach to property appraisal, highlight necessary legal compliances, and facilitate smooth transactions between all involved parties.

- Comparative Market Analysis (CMA): A report used to determine the market value of a property by comparing it to similar properties that have been recently sold, are currently on the market, or were on the market but did not sell within the listing period.

- Purchase Agreement: This legal document outlines the terms and conditions of the sale of the property, including the purchase price, contingencies, and closing date, among other details.

- Loan Application: A form submitted by the borrower to a lender when requesting a mortgage loan. It includes personal and financial information necessary for the lender to make a loan approval decision.

- Appraisal Report: A comprehensive analysis performed by a certified appraiser to determine the estimated market value of a property, usually required by a lender before loan approval.

- Title Report: A document that outlines the history of ownership of the property, including any liens, easements, or other encumbrances that may affect the title's transferability or clarity.

- Home Inspection Report: A detailed account provided by a professional home inspector that assesses the condition of the property and identifies any necessary repairs or maintenance issues.

- Disclosure Statements: Documents in which the seller of a property is required to disclose any known defects or issues with the property that could affect its value or desirability.

Together, these documents form a robust framework to support the decision-making process in real estate transactions, ensuring that all parties have access to detailed and accurate information regarding the property's condition, market value, and legal standing.

Similar forms

The Comparative Market Analysis (CMA) is a document closely related to the Broker Price Opinion (BPO) form, primarily used in real estate to help sellers set listing prices and buyers to make offers on properties. Both documents evaluate current market conditions, assess comparable recently sold properties, and adjust for differences to estimate a property’s value. They share a focus on local market data, including sales trends and inventory levels, to provide an informed estimate of what a property might sell for under current market conditions.

Another document similar to the BPO form is the Real Estate Owned (REO) Property Valuation. This document specifically assesses the value of properties owned by banks or financial institutions as a result of foreclosure or other legal means. Similar to a BPO, it includes an evaluation of the property's condition, marketability, and comparable sales analysis. However, the REO Property Valuation places a stronger emphasis on the condition of the property and potential repairs needed to make it marketable, due to the common issues found with foreclosed properties.

The Appraisal Report is an in-depth analysis used to determine the fair market value of a property, commonly used for mortgage origination. While both the BPO and an appraisal evaluate property condition, market trends, and compare similar property sales, an appraisal is typically more thorough and is conducted by a licensed appraiser. The appraisal process involves a detailed examination of the property’s characteristics, market data, and often includes methodologies not used in a BPO, such as the Cost Approach or Income Approach, in addition to the Sales Comparison Approach.

The Home Inspection Report, while not directly a valuation document, shares similarities with the BPO form in assessing a property's condition. It provides a comprehensive review of the physical structure and mechanical systems of the house, identifying areas that need repair or may pose future problems. Unlike the BPO, which seeks to establish value through market analysis and property condition in the context of selling, the Home Inspection Report is focused on informing the buyer about the condition of the property for informative and negotiation purposes without providing a market value.

Dos and Don'ts

Filling out a Broker Price Opinion (BPO) form is a crucial task that requires attention to detail and accuracy. Adhering to certain dos and don'ts can ensure the process is carried out smoothly. Here are things to keep in mind:

Do:- Gather comprehensive data: Before filling out the form, collect all necessary information regarding the subject property and the comparable sales. This will ensure accuracy in your evaluation.

- Be objective: Strive to maintain an impartial view when evaluating the property's condition, marketability, and value. Your opinion should be based on facts and market data, not personal feelings or interests.

- Provide detailed explanations: When adjustments are made for differences between the subject property and comparables, clearly explain the reasoning behind these adjustments to offer full transparency.

- Review local market conditions: Current market trends play a vital role in determining a property's value. Make sure to accurately assess the general market conditions and reflect these in your analysis.

- Include necessary documentation: If the BPO form requires supplementary documents, such as MLS printouts or photos, ensure these are attached and properly labeled.

- Check for accuracy and completeness: Before submitting, review your BPO form for any inaccuracies or missing information. This final check can prevent delays or the need for revisions.

- Estimate values arbitrarily: Avoid guessing or making assumptions about property values or market conditions without supporting evidence. Your estimates should always be backed by solid data.

- Ignore local factors: Local factors, such as school districts, neighborhood amenities, and zoning regulations, can significantly impact property values. Make sure these elements are considered in your analysis.

- Overlook property flaws: It can be tempting to ignore or minimize issues with the subject property, but full disclosure is crucial. Be honest about any defects or necessary repairs.

- Use outdated comparables: Real estate markets can change rapidly, making it important to use recent sales data in your comparisons. Outdated information can lead to inaccurate valuations.

- Forget to sign the form: A common oversight is forgetting to sign the completed BPO form. Your signature verifies the accuracy of the information provided and complies with regulatory requirements.

- Submit incomplete documentation: Failing to attach all required documents or to provide sufficient detail can result in your BPO being rejected or delayed. Always double-check submission requirements.

Misconceptions

Many misconceptions surround the Broker Price Opinion (BPO) form, impacting both professionals and property owners. Understanding these misconceptions can clarify the BPO's role and value in the real estate market. Here are seven common misunderstandings:

- Equivalence to an Appraisal: A common misconception is that a BPO is equivalent to an appraisal. However, a BPO provides a broker's opinion on the property's value, often for a lower cost and with a quicker turnaround than a formal appraisal. It does not replace the comprehensive evaluation an appraiser provides.

- Legality and Acceptance: Some believe BPOs are not legal or universally accepted. In reality, BPOs are legal in many states and are widely used by banks, lenders, and investors for a variety of purposes, including loan modifications, foreclosures, and short sale approvals.

- Used for Mortgage Applications: There's a misconception that BPOs can be used for mortgage applications. Typically, traditional appraisals are required for new mortgage loans due to their detailed analysis and regulatory compliance. BPOs are generally not accepted for this purpose.

- Cost Equals Quality: Another misunderstanding is that the cost of a BPO directly correlates with its quality. While BPOs are usually less expensive than appraisals, this does not necessarily mean they are of lower quality. BPOs can provide valuable market insights quickly and cost-effectively.

- Only for Distressed Properties: Some assume BPOs are only for distressed properties or foreclosures. Although commonly used in these situations, BPOs can also be beneficial for traditional sales, refinancing, and portfolio management, offering a current market value estimate.

- Comprehensive as Appraisals: It's often believed that a BPO is as comprehensive as an appraisal. While BPOs include market analysis and property comparisons, they do not involve the same level of detailed inspection and are not held to the same standards as appraisals.

- No Qualifications Required for Agents: There's a myth that real estate agents do not need specific qualifications to complete BPOs. In fact, many lenders and companies require agents who perform BPOs to have certain qualifications, such as experience in the market area and understanding of valuation techniques.

Dispelling these misconceptions helps in recognizing the Broker Price Opinion's value and appropriate applications within the real estate industry. It is a useful tool when used correctly and for the right purposes, complementing other forms of property valuation and market analysis.

Key takeaways

Filling out a Broker Price Opinion (BPO) form involves a detailed analysis of a property, its condition, and its surrounding market conditions. This form is a critical tool for assessing property values from a broker's perspective. The following key takeaways are essential for both beginners and seasoned professionals when dealing with a BPO form:

- Accuracy is Crucial: Every piece of information on the BPO needs to be accurate. This includes current market conditions, property specifics, and comparative market analysis. Incorrect information can lead to a faulty valuation.

- Understand Market Conditions: The form segments market conditions into categories such as depressed, slow, stable, and improving. It's important to have a clear understanding of these terms and accurately describe the current market.

- Analyze Comparable Sales: A significant part of the BPO involves comparing the subject property to similar properties that have recently sold. Accurate comparison requires adjustments for differences in size, location, condition, and amenities.

- Detail Required Repairs: Clearly itemizing needed repairs and their costs helps in determining the property's "as is" condition versus its potential marketable condition. This can significantly affect the property's valuation.

- Consider Financing Availability: The availability of financing options for a property can impact its marketability. The form asks whether all types of financing are available for the property, which is a crucial detail to note.

- Marketing Strategy and Expected Time to Sell: The form requires an outline of a marketing strategy and an estimate of the normal marketing time in the area. This helps in setting realistic expectations for the selling process.

- Professional Judgment is Key: While filling out a BPO requires comprehensive data analysis, it also relies on the broker's professional judgment, particularly when making adjustments for comparative properties and assessing overall marketability.

Completing a Broker Price Opinion form is not just about filling in the blanks; it's an intricate process that combines data analysis with professional insight. Understanding these key takeaways helps ensure that the BPO provides a reliable estimation of the property's value, aiding in making informed decisions whether for buying, selling, or lending purposes.

Discover Other PDFs

Lyft Inspection Form Sc - Checking for the presence and functionality of safety equipment, including fire extinguisher and first aid kit.

Employment Eligibility Verification - Often serves as a preliminary step before deeper background or security checks.